Qualifying For Life Insurance With Paralysis [Paraplegic Or Quadriplegic]

Are you currently a paraplegic or quadriplegic? Have you experienced frustration and difficulty trying to get life insurance due to your paralysis?

If you answered “yes” to these questions, then keep reading! Today’s article will focus on…

How To Get Life Insurance if You Have Paralysis as a Paraplegic or Quadriplegic

Before we jump in, let me quickly mention that this article will focus on:

- Hemiplegia,

- Paraplegia,

- Quadriplegia, and,

- Partial paralysis.

Now, let’s get started!

Quick Navigation Article Links:

Can a Paralyzed Individual Qualify for Life Insurance?

The short answer? YES! However, other factors, such as your age, health, and medical history, can greatly affect your insurability.

Plus, before making any decisions, you need to determine what you want your life insurance to accomplish.

Not all life insurance products work the same. While some are ideal at solving permanent financial obligations, others are better at covering “temporary” issues.

Let’s look at a couple of these in more detail.

Here are the Top 5 reasons why people purchase life insurance!

1. Income Replacement

Regardless of your paralysis, you may still earn a substantial amount of income that your loved ones rely on. That’s why it’s understandable that many worry about their families and what would happen if their income disappeared.

Have you ever wondered how your family’s standard of living would hold up? If your family’s finances are a priority, purchasing a life insurance plan is a smart decision.

If you die suddenly, your family will receive a lump sum cash benefit enough to replace your income for a few years during this difficult time.

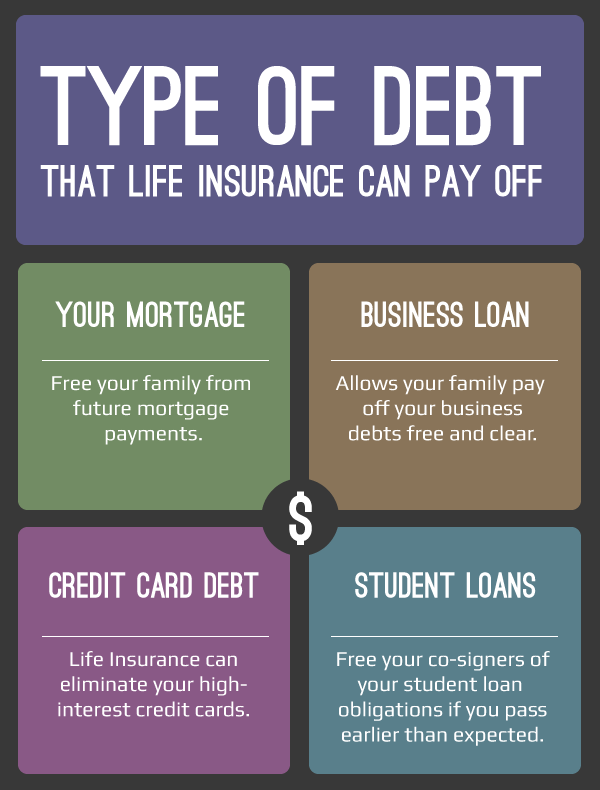

2. Debt Payoff

Many people decide to use life insurance to pay off debt, with their mortgage being a top priority.

Ask yourself whether your family could keep up with the monthly mortgage payments should you pass away… If the answer is no, the bank may force your house into foreclosure, evicting your loved ones in the process.

3. Final Expenses

Do you plan on being buried or cremated? Are you worried that your surviving spouse or kids may have to pay out of pocket for your funeral expenses?

If so, a life insurance plan to cover your final expenses may be worth considering. A life insurance policy provides peace of mind, allowing your family to focus on saying goodbye rather than bickering over who can “afford” to pay your funeral costs.

Life Insurance & Paralysis

Now that we’ve discussed what life insurance can accomplish, let’s look at the types of insurance available.

- Term Life

- Permanent Life (Whole, Universal)

- Guaranteed Acceptance Life Insurance

Term Life Insurance

Term life insurance is temporary life insurance coverage. In short, term life terminates and only lasts a specific amount of time, either 10, 20, or 30 years.

It’s up to you to choose the length of time that suits your temporary need for life insurance.

After your term insurance exceeds the length of coverage, one of either two things will happen:

- Premium Increases

You might be thinking, “that’s alright, a slight increase won’t hurt…” Well, you can forget that because your premium increase could be ten or even 20 times higher than your initial rate.

- Insurance Cancels

No joke! In this situation, if you die only one day AFTER your policy expires, too bad! Your beneficiary won’t receive any money whatsoever.

While this might seem like a rip-off, term insurance does have some advantages and can be a smart choice depending on the situation.

Pro #1 – Level Premiums Payments

The premium rate will remain consistent during the length of the policy. This means nasty NO premium increases!

Pro #2 – Pure Insurance

Unlike permanent life insurance that develops cash value, term insurance sacrifices cash value generation for maximal coverage opportunity.

Term insurance provides the most coverage per dollar of premium[/caption]

What does this mean? Basically, term insurance gives you MORE coverage compared to universal or whole life insurance.

Pro #3 – Ideal for Temporary Obligations

One such temporary obligation that many individuals face is their mortgage or any substantial debt.

A term insurance plan does a good job covering debt because:

- the coverage amount is high enough to provide protection

- the nature of these obligations are temporary

One day you’ll pay off your mortgage, student loans, credit card debt, or save up enough to retire. Therefore, coverage that lasts your entire life isn’t necessary.

Drawbacks #1 – “Man Plans. God Laughs.”

You may NOT reach the savings and retirement goals you had.

Perhaps you hit a bit of a bump and had to readjust your mortgage. Or, maybe the stock market suddenly drops 40% as it did in the Great Recession in 2007, and you fear retiring now isn’t a good idea.

Sometimes our temporary obligations last a little longer than we hoped.

Term Life Insurance Underwriting for the Paralyzed

Term life insurance has stricter underwriting standards across the board.

However, when someone with paralysis, hemiplegia, paraplegia, hemapheresis, and paraphrases applies for life insurance, they will have a better chance of qualifying for term life insurance. But, don’t forget each case is still unique.

What about people with quadriplegia? For quadriplegics, you won’t find anything in the traditional sphere of coverage.

But there are life insurance options for quadriplegics, so stick around.

Term Life Insurance Rates

$100000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-smoker |

|---|---|---|---|---|

| 25 | $17.37 | $8.49 | $15.05 | $6.88 |

| 26 | $17.37 | $8.49 | $15.14 | $6.88 |

| 27 | $17.37 | $8.49 | $15.31 | $6.88 |

| 28 | $17.46 | $8.49 | $15.39 | $6.88 |

| 29 | $17.46 | $8.49 | $15.57 | $6.88 |

| 30 | $17.46 | $8.49 | $15.65 | $6.88 |

| 31 | $18.06 | $8.54 | $16.08 | $6.88 |

| 32 | $18.58 | $8.59 | $16.60 | $6.89 |

| 33 | $19.18 | $8.60 | $17.03 | $7.05 |

| 34 | $19.52 | $8.60 | $17.54 | $7.05 |

| 35 | $19.61 | $8.60 | $17.97 | $7.05 |

| 36 | $20.47 | $8.77 | $18.74 | $7.78 |

| 37 | $21.41 | $9.03 | $19.47 | $8.00 |

| 38 | $22.45 | $9.29 | $20.29 | $8.00 |

| 39 | $23.56 | $9.47 | $21.18 | $8.00 |

| 40 | $24.77 | $9.63 | $22.09 | $8.00 |

| 41 | $26.06 | $10.04 | $23.16 | $9.05 |

| 42 | $27.52 | $10.43 | $24.27 | $9.05 |

| 43 | $29.07 | $10.86 | $25.64 | $9.05 |

| 44 | $30.79 | $11.20 | $27.09 | $9.49 |

| 45 | $32.68 | $11.20 | $28.59 | $9.96 |

| 46 | $34.92 | $12.35 | $30.26 | $10.41 |

| 47 | $37.32 | $12.95 | $32.05 | $10.89 |

| 48 | $40.08 | $13.59 | $34.11 | $11.42 |

| 49 | $43.09 | $14.28 | $36.23 | $12.00 |

| 50 | $45.80 | $15.03 | $38.49 | $12.63 |

| 51 | $49.83 | $15.99 | $41.17 | $13.39 |

| 52 | $54.27 | $17.03 | $44.07 | $14.21 |

| 53 | $58.91 | $18.18 | $47.19 | $15.10 |

| 54 | $64.16 | $19.44 | $50.57 | $16.06 |

| 55 | $70.00 | $20.81 | $54.22 | $17.11 |

| 56 | $75.25 | $22.51 | $58.31 | $18.17 |

| 57 | $81.10 | $24.40 | $62.74 | $19.31 |

| 58 | $90.35 | $26.48 | $67.53 | $21.86 |

| 59 | $98.29 | $28.79 | $72.73 | $23.55 |

| 60 | $106.97 | $31.35 | $78.36 | $25.63 |

| 61 | $116.09 | $34.73 | $85.09 | $27.57 |

| 62 | $126.02 | $38.55 | $92.45 | $29.70 |

| 63 | $131.84 | $41.84 | $125.52 | $41.84 |

| 64 | $143.96 | $47.02 | $135.70 | $46.96 |

| 65 | $157.47 | $52.58 | $142.38 | $46.96 |

| 66 | $173.03 | $58.54 | $165.70 | $58.54 |

| 67 | $190.58 | $64.77 | $182.54 | $64.77 |

| 68 | $210.27 | $71.47 | $185.11 | $68.17 |

| 69 | $232.63 | $79.03 | $206.70 | $75.92 |

| 70 | $257.91 | $87.54 | $230.87 | $75.92 |

| 71 | $286.55 | $97.78 | $257.96 | $94.43 |

| 72 | $319.15 | $109.31 | $288.23 | $103.20 |

| 73 | $356.38 | $121.19 | $353.24 | $121.78 |

| 74 | $398.78 | $138.03 | $398.78 | $132.35 |

| 75 | $447.46 | $155.59 | $402.82 | $145.94 |

$250000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $28.38 | $12.81 | $21.93 | $8.60 |

| 26 | $28.59 | $12.81 | $22.36 | $8.62 |

| 27 | $28.59 | $12.81 | $22.57 | $8.66 |

| 28 | $28.81 | $12.81 | $23.00 | $8.70 |

| 29 | $28.81 | $12.81 | $23.22 | $8.74 |

| 30 | $29.02 | $12.81 | $23.65 | $8.78 |

| 31 | $29.67 | $12.81 | $24.29 | $8.82 |

| 32 | $30.31 | $12.81 | $24.72 | $8.86 |

| 33 | $30.74 | $12.81 | $25.37 | $8.86 |

| 34 | $31.39 | $12.81 | $25.80 | $8.86 |

| 35 | $32.03 | $12.81 | $26.44 | $8.86 |

| 36 | $35.47 | $13.52 | $28.81 | $10.22 |

| 37 | $38.89 | $14.19 | $30.90 | $10.53 |

| 38 | $41.28 | $14.19 | $32.92 | $11.18 |

| 39 | $44.07 | $14.77 | $35.02 | $11.61 |

| 40 | $46.87 | $15.20 | $37.28 | $12.25 |

| 41 | $50.09 | $15.93 | $40.14 | $12.25 |

| 42 | $53.75 | $16.79 | $43.25 | $13.54 |

| 43 | $57.83 | $17.74 | $46.64 | $13.76 |

| 44 | $62.13 | $18.83 | $50.33 | $14.77 |

| 45 | $67.08 | $20.25 | $54.35 | $15.69 |

| 46 | $72.02 | $21.48 | $57.98 | $16.55 |

| 47 | $77.40 | $22.77 | $61.68 | $17.41 |

| 48 | $83.42 | $24.28 | $65.95 | $19.63 |

| 49 | $89.87 | $25.73 | $70.59 | $21.05 |

| 50 | $97.10 | $27.50 | $75.43 | $22.47 |

| 51 | $105.44 | $29.86 | $80.70 | $23.89 |

| 52 | $114.53 | $32.49 | $86.26 | $25.77 |

| 53 | $124.44 | $34.76 | $93.31 | $29.15 |

| 54 | $135.25 | $38.08 | $100.37 | $31.30 |

| 55 | $147.04 | $41.80 | $108.15 | $33.67 |

| 56 | $160.00 | $44.50 | $118.03 | $34.83 |

| 57 | $173.90 | $47.54 | $127.28 | $37.62 |

| 58 | $207.90 | $53.96 | $137.60 | $46.91 |

| 59 | $228.76 | $59.77 | $149.21 | $51.13 |

| 60 | $251.55 | $65.92 | $161.89 | $56.33 |

| 61 | $271.97 | $73.23 | $176.08 | $61.19 |

| 62 | $294.12 | $81.40 | $191.99 | $66.52 |

| 63 | $306.04 | $88.56 | $279.20 | $88.56 |

| 64 | $337.71 | $99.54 | $314.24 | $97.39 |

| 65 | $372.71 | $109.65 | $348.21 | $109.65 |

| 66 | $404.75 | $124.83 | $379.60 | $120.83 |

| 67 | $438.52 | $136.65 | $409.49 | $136.09 |

| 68 | $480.41 | $148.56 | $434.73 | $147.36 |

| 69 | $524.05 | $164.80 | $478.50 | $164.80 |

| 70 | $570.76 | $184.04 | $522.45 | $182.05 |

| 71 | $633.17 | $209.39 | $615.97 | $202.10 |

| 72 | $695.52 | $238.83 | $627.07 | $222.95 |

| 73 | $759.38 | $273.61 | $627.07 | $243.59 |

| 74 | $829.25 | $310.37 | $678.50 | $275.69 |

| 75 | $980.68 | $357.11 | $786.25 | $357.11 |

$500000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $50.31 | $16.77 | $38.70 | $11.95 |

| 26 | $52.03 | $16.77 | $39.56 | $11.95 |

| 27 | $52.03 | $16.77 | $39.99 | $11.95 |

| 28 | $52.03 | $16.85 | $40.60 | $11.95 |

| 29 | $52.03 | $16.87 | $40.85 | $11.95 |

| 30 | $52.03 | $16.87 | $40.85 | $11.95 |

| 31 | $54.18 | $16.87 | $43.43 | $12.10 |

| 32 | $55.47 | $16.87 | $44.26 | $12.19 |

| 33 | $55.90 | $16.87 | $45.07 | $14.19 |

| 34 | $56.33 | $16.87 | $45.89 | $14.19 |

| 35 | $56.33 | $17.48 | $46.50 | $14.62 |

| 36 | $61.06 | $18.42 | $49.07 | $15.05 |

| 37 | $65.36 | $19.50 | $52.49 | $15.91 |

| 38 | $70.09 | $22.14 | $56.33 | $16.77 |

| 39 | $75.03 | $23.65 | $60.18 | $17.63 |

| 40 | $79.98 | $24.94 | $64.88 | $18.49 |

| 41 | $87.43 | $25.80 | $70.09 | $19.78 |

| 42 | $95.03 | $26.66 | $76.44 | $21.07 |

| 43 | $103.20 | $28.81 | $80.70 | $22.12 |

| 44 | $112.23 | $30.53 | $87.11 | $23.56 |

| 45 | $122.55 | $32.25 | $94.38 | $25.41 |

| 46 | $132.01 | $36.12 | $101.22 | $27.15 |

| 47 | $142.76 | $39.13 | $109.34 | $29.03 |

| 48 | $154.80 | $39.13 | $118.75 | $32.46 |

| 49 | $167.70 | $43.34 | $129.01 | $34.61 |

| 50 | $182.32 | $47.64 | $139.81 | $37.19 |

| 51 | $198.66 | $51.38 | $148.67 | $40.76 |

| 52 | $217.15 | $56.67 | $157.12 | $45.06 |

| 53 | $237.36 | $57.16 | $166.41 | $50.22 |

| 54 | $259.96 | $63.10 | $178.02 | $55.04 |

| 55 | $283.04 | $70.26 | $189.63 | $57.62 |

| 56 | $307.28 | $76.69 | $209.32 | $61.92 |

| 57 | $332.50 | $84.11 | $228.97 | $66.65 |

| 58 | $364.13 | $95.46 | $255.20 | $75.59 |

| 59 | $397.05 | $105.35 | $281.66 | $81.18 |

| 60 | $434.67 | $116.53 | $309.81 | $87.63 |

| 61 | $477.42 | $129.43 | $336.31 | $111.47 |

| 62 | $525.39 | $144.05 | $362.27 | $123.62 |

| 63 | $578.40 | $156.61 | $511.27 | $156.61 |

| 64 | $635.68 | $175.47 | $582.22 | $172.00 |

| 65 | $716.11 | $196.72 | $649.73 | $187.05 |

| 66 | $782.74 | $218.18 | $710.14 | $216.29 |

| 67 | $850.71 | $237.25 | $710.14 | $237.25 |

| 68 | $943.40 | $266.73 | $710.14 | $250.99 |

| 69 | $1034.53 | $298.05 | $794.85 | $297.56 |

| 70 | $1136.16 | $333.25 | $889.45 | $333.25 |

| 71 | $1257.61 | $378.21 | $995.66 | $369.37 |

| 72 | $1385.89 | $432.46 | $1114.34 | $405.92 |

| 73 | $1511.45 | $480.93 | $1247.21 | $458.38 |

| 74 | $1651.20 | $557.45 | $1351.83 | $522.02 |

| 75 | $1903.61 | $647.26 | $1549.29 | $538.36 |

$1000000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $85.14 | $31.99 | $67.08 | $18.29 |

| 26 | $85.14 | $31.99 | $68.82 | $18.29 |

| 27 | $85.14 | $31.99 | $70.53 | $18.29 |

| 28 | $85.14 | $31.99 | $70.53 | $19.19 |

| 29 | $85.14 | $31.99 | $72.24 | $19.19 |

| 30 | $85.14 | $31.99 | $72.24 | $19.26 |

| 31 | $87.72 | $32.42 | $75.68 | $19.33 |

| 32 | $90.30 | $32.68 | $77.40 | $19.40 |

| 33 | $92.88 | $32.68 | $77.40 | $24.51 |

| 34 | $95.46 | $33.80 | $79.12 | $25.37 |

| 35 | $98.04 | $34.57 | $81.70 | $25.37 |

| 36 | $106.64 | $34.57 | $87.54 | $25.37 |

| 37 | $116.10 | $34.74 | $94.38 | $27.09 |

| 38 | $124.70 | $41.71 | $102.33 | $28.81 |

| 39 | $134.16 | $44.29 | $109.77 | $30.53 |

| 40 | $142.76 | $47.73 | $119.18 | $33.11 |

| 41 | $158.53 | $51.77 | $128.58 | $35.69 |

| 42 | $174.50 | $51.77 | $141.04 | $36.98 |

| 43 | $192.14 | $51.77 | $153.08 | $40.85 |

| 44 | $211.60 | $60.03 | $165.97 | $43.43 |

| 45 | $233.10 | $66.65 | $180.57 | $46.87 |

| 46 | $252.75 | $71.81 | $195.18 | $50.31 |

| 47 | $274.08 | $77.83 | $209.41 | $54.61 |

| 48 | $297.25 | $79.12 | $220.92 | $58.91 |

| 49 | $322.42 | $86.00 | $237.17 | $62.35 |

| 50 | $349.76 | $92.88 | $255.98 | $69.23 |

| 51 | $383.11 | $103.20 | $273.08 | $75.25 |

| 52 | $419.69 | $106.21 | $291.89 | $81.27 |

| 53 | $462.25 | $106.21 | $314.97 | $93.31 |

| 54 | $503.81 | $118.25 | $339.77 | $104.40 |

| 55 | $552.06 | $134.59 | $367.98 | $115.58 |

| 56 | $600.98 | $147.49 | $396.20 | $123.32 |

| 57 | $654.26 | $161.25 | $428.69 | $131.92 |

| 58 | $712.32 | $186.19 | $502.67 | $142.24 |

| 59 | $775.56 | $205.11 | $568.29 | $154.28 |

| 60 | $844.46 | $227.38 | $632.31 | $166.32 |

| 61 | $927.72 | $254.99 | $672.95 | $229.62 |

| 62 | $1019.23 | $286.81 | $711.99 | $259.72 |

| 63 | $1041.72 | $303.51 | $962.34 | $288.96 |

| 64 | $1155.44 | $340.90 | $1062.10 | $319.06 |

| 65 | $1285.40 | $384.68 | $1152.40 | $349.16 |

| 66 | $1433.31 | $418.30 | $1313.22 | $398.70 |

| 67 | $1601.75 | $458.90 | $1474.04 | $398.70 |

| 68 | $1785.79 | $534.92 | $1612.29 | $398.70 |

| 69 | $1958.65 | $598.99 | $1781.92 | $471.19 |

| 70 | $2151.29 | $674.67 | $1956.50 | $558.40 |

| 71 | $2367.15 | $762.82 | $2201.17 | $632.62 |

| 72 | $2608.81 | $882.36 | $2416.26 | $707.78 |

| 73 | $2880.57 | $1010.07 | $2416.26 | $760.24 |

| 74 | $3185.21 | $1130.47 | $2761.67 | $822.37 |

| 75 | $3488.73 | $1535.93 | $3093.42 | $1234.53 |

Whole Life Insurance

The opposite of term insurance is whole life insurance. Whole life insurance offers permanent protection. Allow me to explain.

1. Coverage NEVER cancels due to age or health

As long as you continue paying your premiums, your coverage can never cancel due to age or health, which is ideal for final expenses.

2. Premiums never increase

Unlike term life insurance premiums, whole life insurance coverage NEVER has premium increases.

Bonus – Universal Life Insurance

Universal life insurance, if set up correctly, can act like whole life insurance. However, designed incorrectly, universal life can run the risk of increasing in price at a future date.

Let me explain.

Sometimes people want a permanent life insurance policy with as much death benefit payout as possible. In this instance, a universal life insurance policy with a “no lapse” clause can do the trick (if they medically qualify).

The way it works is simple. Pay the suggested premium until you pass away, and the policy guarantees to pay out.

However, if you lower the premium (even only for one month), then you lose that privilege and risk having your universal life policy lapse.

Drawbacks #1 – Price

What could possibly be so bad about a policy that never cancels due to age or health? Well, first off, the price.

A permanent life insurance plan is an “upgraded” form of life insurance that comes with a higher premium than term insurance.

Simplified Issue Whole Life

There’s one more permanent product I want to mention before we wrap up our discussion.

If you cannot qualify using a fully underwritten life insurance product, a simplified issue whole life product can help. In short, it’s whole life insurance, meaning the benefits are the same. However, the underwriting standards are not as intense.

For anyone with health issues like paralysis, approval can be MUCH simpler, especially if an illness or disease causes your paralysis.

Burial Insurance Rates With Mutual Of Omaha And Liberty Bankers For $10,000

NOTE: There are more burial insurance coverage options than $10,000. Click the links below to learn more about your options:

$10000 Mutual of Omaha Monthly Rate Chart

| Age | Male. Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 45 | $31.24 | $25.45 | $28.14 | $22.61 |

| 46 | $32.20 | $26.17 | $28.78 | $23.02 |

| 47 | $33.38 | $27.02 | $29.53 | $23.55 |

| 48 | $34.67 | $27.96 | $30.28 | $24.18 |

| 49 | $35.57 | $28.52 | $30.83 | $24.48 |

| 50 | $36.89 | $29.16 | $31.43 | $24.67 |

| 51 | $38.88 | $30.30 | $32.89 | $25.45 |

| 52 | $40.50 | $31.12 | $33.85 | $25.88 |

| 53 | $42.59 | $32.20 | $35.31 | $26.62 |

| 54 | $44.77 | $33.61 | $36.66 | $27.47 |

| 55 | $47.27 | $35.09 | $38.32 | $28.40 |

| 56 | $49.45 | $36.45 | $39.57 | $29.27 |

| 57 | $51.53 | $37.91 | $40.72 | $30.06 |

| 58 | $53.61 | $39.27 | $41.86 | $30.83 |

| 59 | $56.11 | $40.82 | $43.10 | $31.70 |

| 60 | $59.02 | $42.76 | $44.67 | $32.87 |

| 61 | $62.97 | $45.38 | $46.96 | $34.51 |

| 62 | $67.03 | $47.90 | $49.24 | $36.06 |

| 63 | $70.98 | $50.52 | $51.53 | $37.72 |

| 64 | $75.04 | $53.14 | $53.71 | $39.36 |

| 65 | $78.99 | $55.76 | $56.00 | $41.01 |

| 66 | $84.50 | $59.35 | $59.54 | $43.44 |

| 67 | $90.11 | $62.93 | $63.07 | $45.86 |

| 68 | $95.63 | $66.53 | $66.61 | $48.29 |

| 69 | $101.14 | $70.11 | $70.15 | $50.81 |

| 70 | $106.76 | $73.70 | $73.68 | $53.24 |

| 71 | $114.04 | $78.36 | $78.78 | $56.63 |

| 72 | $121.42 | $82.92 | $83.77 | $60.12 |

| 73 | $128.80 | $88.01 | $88.87 | $63.93 |

| 74 | $136.08 | $93.16 | $93.86 | $67.78 |

| 75 | $143.47 | $99.53 | $98.95 | $72.41 |

| 76 | $152.72 | $106.87 | $105.61 | $78.25 |

| 77 | $162.75 | $113.64 | $112.80 | $83.51 |

| 78 | $172.97 | $119.86 | $120.04 | $88.44 |

| 79 | $183.17 | $126.23 | $127.36 | $93.41 |

| 80 | $193.47 | $132.65 | $134.74 | $98.43 |

| 81 | $210.10 | $143.00 | $145.34 | $106.21 |

| 82 | $227.91 | $153.54 | $156.77 | $113.96 |

| 83 | $245.88 | $163.41 | $168.20 | $121.31 |

| 84 | $262.68 | $173.28 | $178.90 | $128.55 |

| 85 | $279.58 | $183.15 | $189.70 | $135.90 |

$10000 Liberty Bankers Life Monthly Rate Chart

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $19.16 | $16.25 | $17.10 | $15.16 |

| 26 | $19.41 | $16.36 | $17.39 | $15.28 |

| 27 | $19.66 | $16.48 | $17.69 | $15.40 |

| 28 | $19.90 | $16.59 | $17.95 | $15.51 |

| 29 | $20.12 | $16.70 | $18.22 | $15.61 |

| 30 | $20.35 | $16.80 | $18.48 | $15.73 |

| 31 | $20.95 | $17.28 | $19.06 | $16.09 |

| 32 | $21.55 | $17.77 | $19.66 | $16.45 |

| 33 | $22.13 | $18.22 | $20.21 | $16.79 |

| 34 | $22.66 | $18.67 | $20.75 | $17.12 |

| 35 | $23.21 | $19.10 | $21.28 | $17.45 |

| 36 | $24.03 | $19.70 | $21.89 | $17.99 |

| 37 | $24.85 | $20.29 | $22.50 | $18.54 |

| 38 | $25.64 | $20.87 | $23.08 | $19.06 |

| 39 | $26.38 | $21.40 | $23.62 | $19.55 |

| 40 | $27.13 | $21.95 | $24.18 | $20.05 |

| 41 | $28.37 | $22.77 | $24.98 | $20.70 |

| 42 | $29.61 | $23.60 | $25.80 | $21.34 |

| 43 | $30.78 | $24.38 | $26.57 | $21.96 |

| 44 | $31.90 | $25.12 | $27.30 | $22.54 |

| 45 | $33.02 | $25.87 | $28.03 | $23.13 |

| 46 | $34.54 | $26.84 | $28.80 | $23.63 |

| 47 | $36.06 | $27.81 | $29.55 | $24.15 |

| 48 | $37.50 | $28.75 | $30.28 | $24.64 |

| 49 | $38.88 | $29.63 | $30.98 | $25.10 |

| 50 | $40.25 | $30.51 | $31.67 | $25.57 |

| 51 | $42.42 | $31.83 | $33.21 | $26.58 |

| 52 | $44.59 | $33.14 | $34.74 | $27.59 |

| 53 | $46.66 | $34.40 | $36.20 | $28.56 |

| 54 | $48.62 | $35.59 | $37.60 | $29.48 |

| 55 | $50.58 | $36.79 | $38.99 | $30.40 |

| 56 | $53.54 | $38.68 | $40.85 | $31.29 |

| 57 | $56.51 | $40.57 | $42.71 | $32.19 |

| 58 | $59.33 | $42.37 | $44.47 | $33.04 |

| 59 | $62.00 | $44.09 | $46.15 | $33.86 |

| 60 | $64.69 | $45.80 | $47.83 | $34.67 |

| 61 | $70.10 | $47.92 | $50.48 | $36.38 |

| 62 | $75.51 | $50.06 | $53.13 | $38.09 |

| 63 | $80.66 | $52.09 | $55.66 | $39.72 |

| 64 | $85.56 | $54.02 | $58.05 | $41.26 |

| 65 | $90.46 | $55.94 | $60.45 | $42.81 |

| 66 | $96.11 | $59.59 | $63.69 | $45.33 |

| 67 | $101.76 | $63.23 | $66.92 | $47.84 |

| 68 | $107.14 | $66.71 | $70.00 | $50.24 |

| 69 | $112.25 | $70.00 | $72.93 | $52.51 |

| 70 | $117.36 | $73.31 | $75.86 | $54.79 |

| 71 | $126.59 | $78.94 | $81.11 | $59.28 |

| 72 | $135.80 | $84.58 | $86.38 | $63.78 |

| 73 | $144.59 | $89.95 | $91.38 | $68.06 |

| 74 | $152.92 | $95.05 | $96.14 | $72.13 |

| 75 | $161.26 | $100.15 | $100.90 | $76.20 |

| 76 | $172.07 | $109.95 | $112.52 | $83.12 |

| 77 | $182.87 | $119.74 | $124.14 | $90.04 |

| 78 | $193.16 | $129.07 | $135.20 | $96.63 |

| 79 | $202.93 | $137.94 | $145.71 | $102.90 |

| 80 | $212.70 | $146.80 | $156.21 | $109.16 |

Case Study – Cremation Coverage with Diabetes Concern

A 45-year-old client named Mr. Howe recently got in touch looking for final expense coverage. He had paraplegia and wanted enough coverage to take care of his cremation costs so that his family wouldn’t be responsible.

In addition to being confined to a wheelchair, Mr. Howe suffered from diabetes. He took insulin regularly and was concerned this would affect his ability to qualify for quality coverage.

The good news is that despite Mr. Howe’s health condition, we were able to help him qualify for first-day full coverage. This is because we have access to multiple insurance carriers.

While I can’t promise the same outcome for everyone, I can promise that we strive to help our clients find affordable quality life insurance coverage at Buy Life Insurance for Burial.

Guaranteed Acceptance

Let’s briefly talk about guaranteed acceptance life insurance.

This insurance product asks ZERO health questions and approves everyone within the specified age range.

Guaranteed life is permanent whole life insurance. It NEVER cancels due to age or health. And there’s NEVER any price increases.

The biggest drawback, however, is that there’s a two-year waiting period for natural death coverage.

This means if you pass away (from natural causes) during this “waiting” period, the policy will only pay out your paid premiums to your beneficiary plus any interest.

Guaranteed Acceptance = Trump Card

As such, guaranteed acceptance life insurance is reserved for folks struggling to find coverage and have been declined by other options. Trust me; I don’t like it either. But unfortunately, there’s no other choice available.

In some cases, certain paralyzed individuals will learn that guaranteed acceptance coverage is their only option.

On the brighter side, you are covered for accidental death from day one! And since these policies are predominantly used for final expense coverage, the maximum is usually $25,000.

But, if you want more, we can add additional policies to increase your coverage.

How To Apply And Next Steps

Let’s say you’ve identified a plan that you think makes sense for you. Here’s what you should do next.

Step #1 – Determine your budget.

Figuring out what you can afford is our topmost priority. Of course, we understand that you wouldn’t want any financial stress whatsoever!

That’s why at Buy Life Insurance For Burial, we always recommend you never bite off more than you can chew.

Step #2 – Pick an agent that can offer you the best price and coverage.

I would like to nominate myself and my team 🙂 At Buy Life Insurance For Burial, we help people find the best combination of price and coverage.

Step #3 – Complete an application for life insurance.

If you work with us, the next step is to tackle your health questions and figure out which carrier will offer you the best life insurance deal.

Assuming you like what you hear, we’d complete an application via email or over the phone. No personal visits are required!

Depending on the policy you apply for, you’ll receive same-day approval. Though in some cases, it may take a few days or weeks.

Next Steps

If you’re ready to discover your options for life or burial insurance, call me at 888-626-0439 now for your free life insurance quote!

Or click here to request a free quote. We will get back to you within the next 24 business hours!

Thank you for reading!