Life Insurance For Siblings [Rates & Companies Revealed]

Are you looking for a quote for burial insurance for siblings? Click here and send me a message with your details. If you’d prefer to speak with me, call 888-626-0439.

Are you interested in getting life insurance for a brother or sister? Do you wonder what the process is for applying and getting approval for burial insurance for siblings?

If so, you’ve found the right website!

Let’s jump right to it!

Quick Navigation Article Links:

- How To Get It

- Why Do It?

- Consent

- No Consent

- Adding Them To Your Policy

- Best Options

- Rates

- How To Buy

- Final Steps

Can You Buy Burial Insurance for Siblings?

The short answer: YES! Many life insurance companies allow brothers and sisters to pay their sibling’s life insurance.

HOWEVER, there are potential obstacles to overcome first. Thankfully, with prior preparation, these landmines won’t cause much fuss.

My goal is to discuss these concerns so you know how to secure the best life insurance plan for your brother or sister.

The truth is that not all life insurance is the same. And some policies can cause HUGE problems if you miss the “fine print.”

So, let’s start by asking ourselves the following questions.

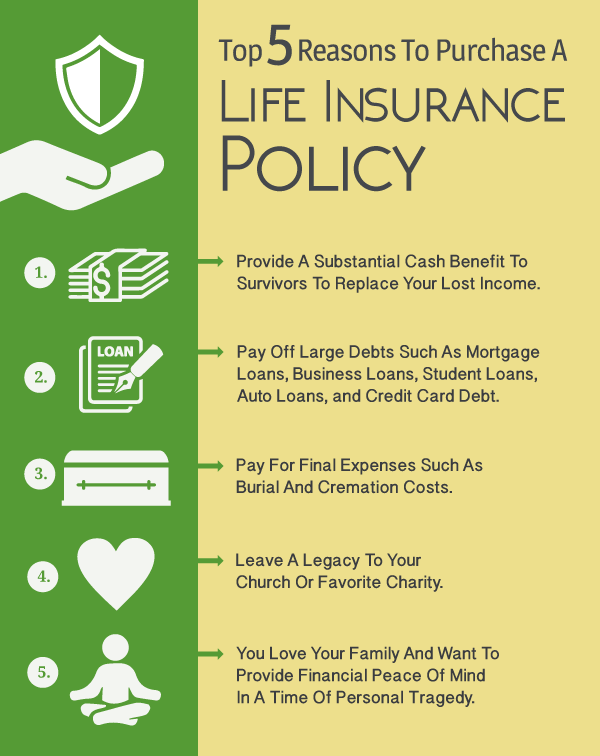

Why Do People Buy Life Insurance On Their Brothers And Sisters?

#1 – Because Their Brother or Sister Isn’t Doing Well Financially

Getting life insurance is an act of love. Why? Because we don’t want our loved ones to suffer.

We don’t want them to shoulder unnecessary burdens. And while life insurance can’t bring back the dead to life… life insurance CAN bring life to the living.

Maybe your sibling isn’t the responsible type, and you know they won’t be financially prepared for burial expenses or other costs should the worst happen.

And of course, you wouldn’t want this financial burden to fall on yourself or another member of your family.

Did you know that the average burial service in 2018, according to the National Funeral Directors Association, costs approximately $8800?

And that’s “average.” It’s common nowadays for funerals to easily exceed $10,000, even $15,000 in total cost. Yikes!

While you may be doing well financially, let me ask you this:

Would coming up with $15,000, even $20,000 to bury your brother or sister “sting” just a little?

That uncomfortable feeling is what motivates many to buy burial insurance for their sibling. At least then, you don’t have to rely on your emergency savings or retirement plan to cover the cost.

#2 – Insuring Your Sibling Is Also About Protecting Your Nieces and Nephews

If your brother or sister passed away, would you feel obligated to help your nieces and nephews?

You can purchase coverage specifically designed to cover your sibling’s earnings. Then you know your nieces and nephews won’t struggle financially during such a difficult time.

#3 – Returning the blessing

Most people I’ve met who’ve done well weren’t born with a silver spoon in their mouth. They’ve worked hard to achieve what they’ve earned!

I’m guessing you’re in the same boat. You’ve sacrificed a lot to get to where you are today. You’re proud of what you’ve accomplished and want to pay it back.

Helping a sibling out by buying burial insurance is the perfect way to do so.

Insured’s Consent And HIPAA

Now let’s shift gears and discuss some of the potential obstacles you’ll face.

HIPAA Consent

The first challenge is gaining consent from your brother or sister to take out life insurance on them.

You see, all life insurance companies require two things to insure an applicant:

- Personal consent of the applicant

- Access to medical records (there are some that DON’T)

Let’s talk about HIPAA.

HIPAA stands for Health Insurance Portability and Accountability Act.

In short, HIPAA requires personal consent from the insured or power of attorney for any entity to access the applicant’s life insurance records.

What does this mean?

Even if you’re 100% on board buying life insurance for a loved one, you STILL require written consent from the insured.

Even your doctor requires your written permission to access your medical records. He CANNOT request those records without your consent or authorization.

Think about it. Do you want some stranger accessing your personal health history? Of course not!

And even though you’re related, the same rule applies when you’re applying for life insurance on a sibling.

Exception – Power of Attorney

The only exception is if you have “power of attorney” for your loved ones. Some insurance companies allow you to sign when you submit proof of this.

There are limitations, though.

My experience with clients with “power of attorney” for a brother or sister is that the sibling’s health is pretty bad off. And while this doesn’t mean there are NO options for coverage, it does mean your options change slightly.

Does This Mean I Take Out Coverage on a Sibling Without Them Knowing?

Maybe your sibling is involved in drugs and doesn’t take care of themselves. Whatever the situation, you worry all the time that something terrible could happen!

Of course, it would be easier to sort things out without them know but…

It’s easier than you think to get your brother or sister’s consent.

In my experience, most siblings will be open-minded to getting life insurance coverage.

Just be honest! Have a sit down with your sibling. Explain why you want to get life insurance for them and that you’re not trying to make money from them dying.

Emphasize that you LOVE them and want to ensure their final expenses are taken care of.

If they grumble, tell them there are endless stories of families torn apart because they argued over who pays for what when someone dies. And taking out life insurance is the solution to this risk.

Of course, tell them that you’ll be paying for it 🙂 Lead with that if you think it will help!

HONESTY IS THE BEST POLICY!

They may not like the idea, but with enough effort, you can change their mind.

The key is to connect the cost of their death with the type of burden it would cause you and the family.

What if My Sibling Is Not Close by to Sign off on the Life Insurance Policy?

Most life insurance plans only need recorded verbal consent or a digital signature. Worst case, we can mail your sibling the paperwork.

We here at Buy Life Insurance For Burial operate entirely over the phone and through email. So there’s no need to worry!

Can You Put Your Sibling On Your Existing Life Insurance Plan?

Unfortunately, no. Both life insurance through work and a personal policy is only valid for immediate family members, such as your spouse and children.

Simply put, life insurance companies require a separate life insurance application on him to determine insurability.

What Is The Best Life Insurance Policy For My Sibling?

“BEST” is subjective and depends on each individual’s situation.

You must determine why you want coverage to determine what’s best for your sibling. And NO one-type policy will be the best option across the board for everyone!

There’s a variety of life insurance products available. Let’s take a look!

#1 – Final Expense Protection

Burial costs are a permanent concern. You don’t know when your brother or sister will die. That’s why a final expense burial insurance policy makes sense.

It’s permanent protection, meaning it CANNOT cancel due to age or health. And in most cases, the premium will NEVER increase.

#2 – Protect Your Sibling’s Home

One great reason to purchase life insurance on a sibling is to eliminate their mortgage if they pass away before paying it off.

A mortgage is a temporary concern. So a 20-year or 30-year term life insurance plan is perfect in this situation.

#3 – Joint Debt or Business

Do you and your sibling have mutual debt?

What happens if your brother or sister dies before paying it off? Most likely, covering your sibling’s half of the debt will fall on your shoulders.

Perhaps you’re business partners and have a loan you need to be covered, or you’re looking for a way to buy out one another if you jointly own a business together.

Here’s the bottom line…

LIFE INSURANCE = PROTECTION FOR YOU AND YOUR FAMILY

A life insurance policy provides a lump sum death benefit to the family of your sibling. It protects his or her loved ones in times of financial strife.

Best Companies And Rates

The next step is to determine what TYPE of coverage serves you best. To an extent, which type of policy you’ll select depends on how healthy your brother or sister is.

Sibling Is in Good Health

Let’s say your sibling is in really good health. No significant health issues, but maybe takes a high blood pressure pill. Nothing major.

Understandably, if you want to cover funeral costs, you’ll want a permanent solution, right?

It makes sense to purchase life insurance to cover a sibling’s whole life, right? For that, a whole life insurance product works perfectly.

A whole life insurance plan lasts your whole life, and can NEVER cancel due to age or health. Let’s look at some of the other benefits!

Benefit #1 – Rates Never Increase.

With whole life insurance, your rates NEVER go up. The first payment is identical to the LAST!

If you HATE life insurance premiums that increase, you’ll LOVE whole life insurance.

Benefit #2 – Can’t Be Cancelled Due To Age Or Health

As we mentioned above, your sibling’s life insurance coverage CANNOT cancel due to age or health.

Benefit #3 – May Qualify For 1st Day Full Coverage

If medically approved, your sibling could qualify for first-day full natural and accidental death!

Unlike guaranteed acceptance life insurance policies made for people with poor health, your brother or sister is FULLY covered for the ENTIRE amount.

Benefit #4 – Flexible Coverage

You can secure a plan as low as $1,000 or as high as $100,000 or more!

Are you more concerned about paying off significant amounts of debt, such as a mortgage or loan? For that, a term insurance plan makes more sense.

Term insurance offers more premium coverage for your dollar and is perfect for temporary problems! Just be aware of the following:

Insurance companies purposely create term life policies to (a) cancel at their expiration date or (b) increase substantially in price at a future date.

Sibling Is in OK Health

Maybe they have heart disease, diabetes, or some other chronic illness. Their health isn’t BAD, but it isn’t good, either. Then you should look at:

Simplified Issue Whole Life Insurance

Simplified issue whole life insurance is much easier to qualify for.

Benefit #1 – No Exam

First, a simplified issue life insurance product does not require a medical exam.

Benefit #2 – Speed

Decisions on applications for life insurance are quick. Some companies offer same-day approval. Others take 1-2 weeks.

Recently I approved a couple for a simplified issue whole life insurance policy. Within seven days, they were not only approved, but they also had their policies in hand. That’s lickedy-split!

Why is simplified issue so much faster?

It’s because there’s minimal underwriting.

[Biggest] Benefit #3 – Ease Of Issue

Life insurance companies with simplified issue products usually look at your medical records on the MIB and check your prescriptions history to determine insurability.

This is a significant advantage because if your sibling couldn’t qualify for a traditional life insurance plan, they will have a higher chance of getting approved with simplified issue whole life insurance.

Let’s imagine your brother or sister had cancer five years ago.

Most simplified issue whole life insurance plans only look at the last 2 or 3 years on cancer history, meaning not only would your sibling be approved, but they would qualify for preferred rates!

This is in contrast to fully underwritten life insurance (aka traditional policy).

A fully underwritten company MAY offer insurance to your sibling but only after a grueling physical and invasive Q&A from the life insurance underwriters.

And there’s no promise that the quoted price may stay the same.

Benefit #4 – Same Benefits As Whole Life

Simplified issue whole life NEVER has rate increases, coverage NEVER cancels due to age or health, and you may qualify for first-day full coverage for natural and accidental death. Even with health history issues, too!

There’s also simplified issue TERM life insurance as well.

If clearing your sibling’s debt or supporting their family is your concern, a non-med term insurance plan may be the way to go.

Like a simplified issue whole life insurance plan, there’s no examination. And the underwriting is relaxed compared to fully underwritten life insurance.

Remember, though, a simplified issue whole life plan is usually EASIER to qualify for a simplified issue term life plan.

Sibling Is in Really Bad Health

Let’s say you’ve got a sibling with cancer or who’s had recent cardiac problems. Perhaps they’re disabled and had to take retirement early.

Is it possible to get any kind of life insurance coverage on your sibling?

YES, you can! Even if they are terminal or in terrible health.

Guaranteed Acceptance Life Insurance For Siblings

Guaranteed Acceptance = Special Simplified Issue Whole Life

Guaranteed acceptance life insurance is basically the MOST simplified, simplified issue whole life insurance.

Here’s why.

First, rates never go up, and coverage can’t cancel due to age your health.

No health questions asked – the application asks no health questions. Zero, nada!

However, all guaranteed acceptance policies require a minimum two-year waiting period for full payment for natural causes of death. Some companies will make you wait for three or four years!

Either way, we at Buy Life Insurance For Burial treat guaranteed acceptance plans as a last-ditch effort. If no other policy accepts your sibling, then we look at guaranteed issue coverage.

However, naturally, we can’t provide an underwriting assessment without talking to you or your sibling first.

But I can tell you that some people have been shocked at what they can qualify for despite their health history. This is why you should talk to me.

Call me at 888-626-0439!

Term Life Insurance Rates For Siblings

Let’s look at sample rates from Banner Life for 10-year term life insurance coverage.

$100000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-smoker |

|---|---|---|---|---|

| 25 | $17.37 | $8.49 | $15.05 | $6.88 |

| 26 | $17.37 | $8.49 | $15.14 | $6.88 |

| 27 | $17.37 | $8.49 | $15.31 | $6.88 |

| 28 | $17.46 | $8.49 | $15.39 | $6.88 |

| 29 | $17.46 | $8.49 | $15.57 | $6.88 |

| 30 | $17.46 | $8.49 | $15.65 | $6.88 |

| 31 | $18.06 | $8.54 | $16.08 | $6.88 |

| 32 | $18.58 | $8.59 | $16.60 | $6.89 |

| 33 | $19.18 | $8.60 | $17.03 | $7.05 |

| 34 | $19.52 | $8.60 | $17.54 | $7.05 |

| 35 | $19.61 | $8.60 | $17.97 | $7.05 |

| 36 | $20.47 | $8.77 | $18.74 | $7.78 |

| 37 | $21.41 | $9.03 | $19.47 | $8.00 |

| 38 | $22.45 | $9.29 | $20.29 | $8.00 |

| 39 | $23.56 | $9.47 | $21.18 | $8.00 |

| 40 | $24.77 | $9.63 | $22.09 | $8.00 |

| 41 | $26.06 | $10.04 | $23.16 | $9.05 |

| 42 | $27.52 | $10.43 | $24.27 | $9.05 |

| 43 | $29.07 | $10.86 | $25.64 | $9.05 |

| 44 | $30.79 | $11.20 | $27.09 | $9.49 |

| 45 | $32.68 | $11.20 | $28.59 | $9.96 |

| 46 | $34.92 | $12.35 | $30.26 | $10.41 |

| 47 | $37.32 | $12.95 | $32.05 | $10.89 |

| 48 | $40.08 | $13.59 | $34.11 | $11.42 |

| 49 | $43.09 | $14.28 | $36.23 | $12.00 |

| 50 | $45.80 | $15.03 | $38.49 | $12.63 |

| 51 | $49.83 | $15.99 | $41.17 | $13.39 |

| 52 | $54.27 | $17.03 | $44.07 | $14.21 |

| 53 | $58.91 | $18.18 | $47.19 | $15.10 |

| 54 | $64.16 | $19.44 | $50.57 | $16.06 |

| 55 | $70.00 | $20.81 | $54.22 | $17.11 |

| 56 | $75.25 | $22.51 | $58.31 | $18.17 |

| 57 | $81.10 | $24.40 | $62.74 | $19.31 |

| 58 | $90.35 | $26.48 | $67.53 | $21.86 |

| 59 | $98.29 | $28.79 | $72.73 | $23.55 |

| 60 | $106.97 | $31.35 | $78.36 | $25.63 |

| 61 | $116.09 | $34.73 | $85.09 | $27.57 |

| 62 | $126.02 | $38.55 | $92.45 | $29.70 |

| 63 | $131.84 | $41.84 | $125.52 | $41.84 |

| 64 | $143.96 | $47.02 | $135.70 | $46.96 |

| 65 | $157.47 | $52.58 | $142.38 | $46.96 |

| 66 | $173.03 | $58.54 | $165.70 | $58.54 |

| 67 | $190.58 | $64.77 | $182.54 | $64.77 |

| 68 | $210.27 | $71.47 | $185.11 | $68.17 |

| 69 | $232.63 | $79.03 | $206.70 | $75.92 |

| 70 | $257.91 | $87.54 | $230.87 | $75.92 |

| 71 | $286.55 | $97.78 | $257.96 | $94.43 |

| 72 | $319.15 | $109.31 | $288.23 | $103.20 |

| 73 | $356.38 | $121.19 | $353.24 | $121.78 |

| 74 | $398.78 | $138.03 | $398.78 | $132.35 |

| 75 | $447.46 | $155.59 | $402.82 | $145.94 |

$250000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $28.38 | $12.81 | $21.93 | $8.60 |

| 26 | $28.59 | $12.81 | $22.36 | $8.62 |

| 27 | $28.59 | $12.81 | $22.57 | $8.66 |

| 28 | $28.81 | $12.81 | $23.00 | $8.70 |

| 29 | $28.81 | $12.81 | $23.22 | $8.74 |

| 30 | $29.02 | $12.81 | $23.65 | $8.78 |

| 31 | $29.67 | $12.81 | $24.29 | $8.82 |

| 32 | $30.31 | $12.81 | $24.72 | $8.86 |

| 33 | $30.74 | $12.81 | $25.37 | $8.86 |

| 34 | $31.39 | $12.81 | $25.80 | $8.86 |

| 35 | $32.03 | $12.81 | $26.44 | $8.86 |

| 36 | $35.47 | $13.52 | $28.81 | $10.22 |

| 37 | $38.89 | $14.19 | $30.90 | $10.53 |

| 38 | $41.28 | $14.19 | $32.92 | $11.18 |

| 39 | $44.07 | $14.77 | $35.02 | $11.61 |

| 40 | $46.87 | $15.20 | $37.28 | $12.25 |

| 41 | $50.09 | $15.93 | $40.14 | $12.25 |

| 42 | $53.75 | $16.79 | $43.25 | $13.54 |

| 43 | $57.83 | $17.74 | $46.64 | $13.76 |

| 44 | $62.13 | $18.83 | $50.33 | $14.77 |

| 45 | $67.08 | $20.25 | $54.35 | $15.69 |

| 46 | $72.02 | $21.48 | $57.98 | $16.55 |

| 47 | $77.40 | $22.77 | $61.68 | $17.41 |

| 48 | $83.42 | $24.28 | $65.95 | $19.63 |

| 49 | $89.87 | $25.73 | $70.59 | $21.05 |

| 50 | $97.10 | $27.50 | $75.43 | $22.47 |

| 51 | $105.44 | $29.86 | $80.70 | $23.89 |

| 52 | $114.53 | $32.49 | $86.26 | $25.77 |

| 53 | $124.44 | $34.76 | $93.31 | $29.15 |

| 54 | $135.25 | $38.08 | $100.37 | $31.30 |

| 55 | $147.04 | $41.80 | $108.15 | $33.67 |

| 56 | $160.00 | $44.50 | $118.03 | $34.83 |

| 57 | $173.90 | $47.54 | $127.28 | $37.62 |

| 58 | $207.90 | $53.96 | $137.60 | $46.91 |

| 59 | $228.76 | $59.77 | $149.21 | $51.13 |

| 60 | $251.55 | $65.92 | $161.89 | $56.33 |

| 61 | $271.97 | $73.23 | $176.08 | $61.19 |

| 62 | $294.12 | $81.40 | $191.99 | $66.52 |

| 63 | $306.04 | $88.56 | $279.20 | $88.56 |

| 64 | $337.71 | $99.54 | $314.24 | $97.39 |

| 65 | $372.71 | $109.65 | $348.21 | $109.65 |

| 66 | $404.75 | $124.83 | $379.60 | $120.83 |

| 67 | $438.52 | $136.65 | $409.49 | $136.09 |

| 68 | $480.41 | $148.56 | $434.73 | $147.36 |

| 69 | $524.05 | $164.80 | $478.50 | $164.80 |

| 70 | $570.76 | $184.04 | $522.45 | $182.05 |

| 71 | $633.17 | $209.39 | $615.97 | $202.10 |

| 72 | $695.52 | $238.83 | $627.07 | $222.95 |

| 73 | $759.38 | $273.61 | $627.07 | $243.59 |

| 74 | $829.25 | $310.37 | $678.50 | $275.69 |

| 75 | $980.68 | $357.11 | $786.25 | $357.11 |

$500000 Banner Term Insurance Monthly Rate Chart – 10 Year Term

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $50.31 | $16.77 | $38.70 | $11.95 |

| 26 | $52.03 | $16.77 | $39.56 | $11.95 |

| 27 | $52.03 | $16.77 | $39.99 | $11.95 |

| 28 | $52.03 | $16.85 | $40.60 | $11.95 |

| 29 | $52.03 | $16.87 | $40.85 | $11.95 |

| 30 | $52.03 | $16.87 | $40.85 | $11.95 |

| 31 | $54.18 | $16.87 | $43.43 | $12.10 |

| 32 | $55.47 | $16.87 | $44.26 | $12.19 |

| 33 | $55.90 | $16.87 | $45.07 | $14.19 |

| 34 | $56.33 | $16.87 | $45.89 | $14.19 |

| 35 | $56.33 | $17.48 | $46.50 | $14.62 |

| 36 | $61.06 | $18.42 | $49.07 | $15.05 |

| 37 | $65.36 | $19.50 | $52.49 | $15.91 |

| 38 | $70.09 | $22.14 | $56.33 | $16.77 |

| 39 | $75.03 | $23.65 | $60.18 | $17.63 |

| 40 | $79.98 | $24.94 | $64.88 | $18.49 |

| 41 | $87.43 | $25.80 | $70.09 | $19.78 |

| 42 | $95.03 | $26.66 | $76.44 | $21.07 |

| 43 | $103.20 | $28.81 | $80.70 | $22.12 |

| 44 | $112.23 | $30.53 | $87.11 | $23.56 |

| 45 | $122.55 | $32.25 | $94.38 | $25.41 |

| 46 | $132.01 | $36.12 | $101.22 | $27.15 |

| 47 | $142.76 | $39.13 | $109.34 | $29.03 |

| 48 | $154.80 | $39.13 | $118.75 | $32.46 |

| 49 | $167.70 | $43.34 | $129.01 | $34.61 |

| 50 | $182.32 | $47.64 | $139.81 | $37.19 |

| 51 | $198.66 | $51.38 | $148.67 | $40.76 |

| 52 | $217.15 | $56.67 | $157.12 | $45.06 |

| 53 | $237.36 | $57.16 | $166.41 | $50.22 |

| 54 | $259.96 | $63.10 | $178.02 | $55.04 |

| 55 | $283.04 | $70.26 | $189.63 | $57.62 |

| 56 | $307.28 | $76.69 | $209.32 | $61.92 |

| 57 | $332.50 | $84.11 | $228.97 | $66.65 |

| 58 | $364.13 | $95.46 | $255.20 | $75.59 |

| 59 | $397.05 | $105.35 | $281.66 | $81.18 |

| 60 | $434.67 | $116.53 | $309.81 | $87.63 |

| 61 | $477.42 | $129.43 | $336.31 | $111.47 |

| 62 | $525.39 | $144.05 | $362.27 | $123.62 |

| 63 | $578.40 | $156.61 | $511.27 | $156.61 |

| 64 | $635.68 | $175.47 | $582.22 | $172.00 |

| 65 | $716.11 | $196.72 | $649.73 | $187.05 |

| 66 | $782.74 | $218.18 | $710.14 | $216.29 |

| 67 | $850.71 | $237.25 | $710.14 | $237.25 |

| 68 | $943.40 | $266.73 | $710.14 | $250.99 |

| 69 | $1034.53 | $298.05 | $794.85 | $297.56 |

| 70 | $1136.16 | $333.25 | $889.45 | $333.25 |

| 71 | $1257.61 | $378.21 | $995.66 | $369.37 |

| 72 | $1385.89 | $432.46 | $1114.34 | $405.92 |

| 73 | $1511.45 | $480.93 | $1247.21 | $458.38 |

| 74 | $1651.20 | $557.45 | $1351.83 | $522.02 |

| 75 | $1903.61 | $647.26 | $1549.29 | $538.36 |

Simplified Issue Whole Life Cost (For Final Expense Coverage)

To keep our comparisons simple, let’s look at $10,000 in coverage with Mutual Of Omaha and Liberty Bankers Life.

If you want MORE or LESS than $10,000, you can click on the following links below to see premium rates for:

Now, let’s look at what $10,000 in burial insurance runs at:

$10000 Mutual of Omaha Monthly Rate Chart

| Age | Male. Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 45 | $31.24 | $25.45 | $28.14 | $22.61 |

| 46 | $32.20 | $26.17 | $28.78 | $23.02 |

| 47 | $33.38 | $27.02 | $29.53 | $23.55 |

| 48 | $34.67 | $27.96 | $30.28 | $24.18 |

| 49 | $35.57 | $28.52 | $30.83 | $24.48 |

| 50 | $36.89 | $29.16 | $31.43 | $24.67 |

| 51 | $38.88 | $30.30 | $32.89 | $25.45 |

| 52 | $40.50 | $31.12 | $33.85 | $25.88 |

| 53 | $42.59 | $32.20 | $35.31 | $26.62 |

| 54 | $44.77 | $33.61 | $36.66 | $27.47 |

| 55 | $47.27 | $35.09 | $38.32 | $28.40 |

| 56 | $49.45 | $36.45 | $39.57 | $29.27 |

| 57 | $51.53 | $37.91 | $40.72 | $30.06 |

| 58 | $53.61 | $39.27 | $41.86 | $30.83 |

| 59 | $56.11 | $40.82 | $43.10 | $31.70 |

| 60 | $59.02 | $42.76 | $44.67 | $32.87 |

| 61 | $62.97 | $45.38 | $46.96 | $34.51 |

| 62 | $67.03 | $47.90 | $49.24 | $36.06 |

| 63 | $70.98 | $50.52 | $51.53 | $37.72 |

| 64 | $75.04 | $53.14 | $53.71 | $39.36 |

| 65 | $78.99 | $55.76 | $56.00 | $41.01 |

| 66 | $84.50 | $59.35 | $59.54 | $43.44 |

| 67 | $90.11 | $62.93 | $63.07 | $45.86 |

| 68 | $95.63 | $66.53 | $66.61 | $48.29 |

| 69 | $101.14 | $70.11 | $70.15 | $50.81 |

| 70 | $106.76 | $73.70 | $73.68 | $53.24 |

| 71 | $114.04 | $78.36 | $78.78 | $56.63 |

| 72 | $121.42 | $82.92 | $83.77 | $60.12 |

| 73 | $128.80 | $88.01 | $88.87 | $63.93 |

| 74 | $136.08 | $93.16 | $93.86 | $67.78 |

| 75 | $143.47 | $99.53 | $98.95 | $72.41 |

| 76 | $152.72 | $106.87 | $105.61 | $78.25 |

| 77 | $162.75 | $113.64 | $112.80 | $83.51 |

| 78 | $172.97 | $119.86 | $120.04 | $88.44 |

| 79 | $183.17 | $126.23 | $127.36 | $93.41 |

| 80 | $193.47 | $132.65 | $134.74 | $98.43 |

| 81 | $210.10 | $143.00 | $145.34 | $106.21 |

| 82 | $227.91 | $153.54 | $156.77 | $113.96 |

| 83 | $245.88 | $163.41 | $168.20 | $121.31 |

| 84 | $262.68 | $173.28 | $178.90 | $128.55 |

| 85 | $279.58 | $183.15 | $189.70 | $135.90 |

$10000 Liberty Bankers Life Monthly Rate Chart

| Age | Male, Smoker | Male, Non-Smoker | Female, Smoker | Female, Non-Smoker |

|---|---|---|---|---|

| 25 | $19.16 | $16.25 | $17.10 | $15.16 |

| 26 | $19.41 | $16.36 | $17.39 | $15.28 |

| 27 | $19.66 | $16.48 | $17.69 | $15.40 |

| 28 | $19.90 | $16.59 | $17.95 | $15.51 |

| 29 | $20.12 | $16.70 | $18.22 | $15.61 |

| 30 | $20.35 | $16.80 | $18.48 | $15.73 |

| 31 | $20.95 | $17.28 | $19.06 | $16.09 |

| 32 | $21.55 | $17.77 | $19.66 | $16.45 |

| 33 | $22.13 | $18.22 | $20.21 | $16.79 |

| 34 | $22.66 | $18.67 | $20.75 | $17.12 |

| 35 | $23.21 | $19.10 | $21.28 | $17.45 |

| 36 | $24.03 | $19.70 | $21.89 | $17.99 |

| 37 | $24.85 | $20.29 | $22.50 | $18.54 |

| 38 | $25.64 | $20.87 | $23.08 | $19.06 |

| 39 | $26.38 | $21.40 | $23.62 | $19.55 |

| 40 | $27.13 | $21.95 | $24.18 | $20.05 |

| 41 | $28.37 | $22.77 | $24.98 | $20.70 |

| 42 | $29.61 | $23.60 | $25.80 | $21.34 |

| 43 | $30.78 | $24.38 | $26.57 | $21.96 |

| 44 | $31.90 | $25.12 | $27.30 | $22.54 |

| 45 | $33.02 | $25.87 | $28.03 | $23.13 |

| 46 | $34.54 | $26.84 | $28.80 | $23.63 |

| 47 | $36.06 | $27.81 | $29.55 | $24.15 |

| 48 | $37.50 | $28.75 | $30.28 | $24.64 |

| 49 | $38.88 | $29.63 | $30.98 | $25.10 |

| 50 | $40.25 | $30.51 | $31.67 | $25.57 |

| 51 | $42.42 | $31.83 | $33.21 | $26.58 |

| 52 | $44.59 | $33.14 | $34.74 | $27.59 |

| 53 | $46.66 | $34.40 | $36.20 | $28.56 |

| 54 | $48.62 | $35.59 | $37.60 | $29.48 |

| 55 | $50.58 | $36.79 | $38.99 | $30.40 |

| 56 | $53.54 | $38.68 | $40.85 | $31.29 |

| 57 | $56.51 | $40.57 | $42.71 | $32.19 |

| 58 | $59.33 | $42.37 | $44.47 | $33.04 |

| 59 | $62.00 | $44.09 | $46.15 | $33.86 |

| 60 | $64.69 | $45.80 | $47.83 | $34.67 |

| 61 | $70.10 | $47.92 | $50.48 | $36.38 |

| 62 | $75.51 | $50.06 | $53.13 | $38.09 |

| 63 | $80.66 | $52.09 | $55.66 | $39.72 |

| 64 | $85.56 | $54.02 | $58.05 | $41.26 |

| 65 | $90.46 | $55.94 | $60.45 | $42.81 |

| 66 | $96.11 | $59.59 | $63.69 | $45.33 |

| 67 | $101.76 | $63.23 | $66.92 | $47.84 |

| 68 | $107.14 | $66.71 | $70.00 | $50.24 |

| 69 | $112.25 | $70.00 | $72.93 | $52.51 |

| 70 | $117.36 | $73.31 | $75.86 | $54.79 |

| 71 | $126.59 | $78.94 | $81.11 | $59.28 |

| 72 | $135.80 | $84.58 | $86.38 | $63.78 |

| 73 | $144.59 | $89.95 | $91.38 | $68.06 |

| 74 | $152.92 | $95.05 | $96.14 | $72.13 |

| 75 | $161.26 | $100.15 | $100.90 | $76.20 |

| 76 | $172.07 | $109.95 | $112.52 | $83.12 |

| 77 | $182.87 | $119.74 | $124.14 | $90.04 |

| 78 | $193.16 | $129.07 | $135.20 | $96.63 |

| 79 | $202.93 | $137.94 | $145.71 | $102.90 |

| 80 | $212.70 | $146.80 | $156.21 | $109.16 |

Guaranteed Acceptance Whole Life Quotes For Siblings

Let’s say your sibling is in BAD health. And you seriously DOUBT he or she will qualify for any life insurance. The good news is that I can help!

I have access to guaranteed issue life insurance coverage with AIG that asks ZERO health questions and qualifies ANYONE for coverage between the ages of 50 and 85.

I also have access to carriers that ask minimal to NO health questions if your sibling is UNDER 50 years old and in BAD health. Contact me here to find out more.

Let’s take a look at pricing with AIG.

$5000 AIG Monthly Rate Chart

| Age | Male | Female |

|---|---|---|

| 51 | $26.96 | $18.92 |

| 52 | $27.36 | $18.93 |

| 53 | $27.82 | $20.00 |

| 54 | $28.22 | $20.97 |

| 55 | $28.68 | $21.84 |

| 56 | $29.45 | $22.62 |

| 57 | $30.27 | $23.49 |

| 58 | $30.98 | $24.17 |

| 59 | $31.65 | $24.86 |

| 60 | $32.10 | $25.50 |

| 61 | $32.58 | $26.01 |

| 62 | $34.77 | $27.52 |

| 63 | $36.97 | $28.90 |

| 64 | $39.08 | $30.09 |

| 65 | $41.10 | $31.00 |

| 66 | $43.08 | $31.78 |

| 67 | $44.81 | $33.40 |

| 68 | $46.33 | $35.96 |

| 69 | $47.75 | $37.16 |

| 70 | $48.99 | $38.26 |

| 71 | $50.09 | $41.93 |

| 72 | $54.59 | $45.42 |

| 73 | $58.99 | $48.76 |

| 74 | $58.99 | $51.83 |

| 75 | $66.97 | $54.59 |

| 76 | $70.28 | $62.38 |

| 77 | $81.97 | $69.73 |

| 78 | $93.20 | $76.60 |

| 79 | $103.98 | $83.02 |

| 80 | $114.31 | $88.71 |

| 81 | $124.22 | $90.69 |

| 82 | $127.59 | $92.83 |

| 83 | $131.19 | $95.83 |

| 84 | $145.08 | $98.17 |

| 85 | $151.97 | $100.53 |

$10000 AIG Monthly Rate Chart

| Age | Male | Female |

|---|---|---|

| 50 | $51.92 | $35.83 |

| 51 | $52.73 | $36.68 |

| 52 | $53.63 | $37.99 |

| 53 | $54.44 | $39.93 |

| 54 | $55.36 | $41.67 |

| 55 | $56.90 | $43.23 |

| 56 | $58.55 | $44.98 |

| 57 | $60.01 | $46.34 |

| 58 | $61.31 | $47.72 |

| 59 | $62.21 | $49.00 |

| 60 | $63.17 | $50.02 |

| 61 | $67.54 | $53.04 |

| 62 | $71.94 | $55.80 |

| 63 | $76.16 | $58.19 |

| 64 | $80.21 | $60.01 |

| 65 | $84.15 | $61.57 |

| 66 | $87.63 | $64.79 |

| 67 | $90.66 | $67.45 |

| 68 | $93.49 | $69.91 |

| 69 | $95.98 | $72.32 |

| 70 | $98.18 | $74.52 |

| 71 | $107.17 | $81.85 |

| 72 | $115.98 | $88.83 |

| 73 | $124.24 | $95.52 |

| 74 | $131.95 | $101.66 |

| 75 | $138.55 | $107.17 |

| 76 | $161.93 | $122.76 |

| 77 | $184.41 | $137.45 |

| 78 | $205.96 | $151.20 |

| 79 | $226.62 | $164.05 |

| 80 | $246.44 | $175.42 |

| 81 | $253.19 | $179.39 |

| 82 | $260.38 | $183.66 |

| 83 | $288.16 | $189.65 |

| 84 | $301.93 | $194.33 |

| 85 | $315.82 | $199.06 |

$15000 AIG Monthly Rate Chart

| Age | Male | Female |

|---|---|---|

| 50 | $76.89 | $52.74 |

| 51 | $78.09 | $54.02 |

| 52 | $79.45 | $55.98 |

| 53 | $80.66 | $58.90 |

| 54 | $82.04 | $61.51 |

| 55 | $84.35 | $63.85 |

| 56 | $86.82 | $66.47 |

| 57 | $89.01 | $68.50 |

| 58 | $90.96 | $70.58 |

| 59 | $92.31 | $72.50 |

| 60 | $93.75 | $74.03 |

| 61 | $100.31 | $78.56 |

| 62 | $106.91 | $82.70 |

| 63 | $113.24 | $86.28 |

| 64 | $119.31 | $89.01 |

| 65 | $125.23 | $91.35 |

| 66 | $130.44 | $96.19 |

| 67 | $134.98 | $100.18 |

| 68 | $139.24 | $103.87 |

| 69 | $142.96 | $107.47 |

| 70 | $146.27 | $110.78 |

| 71 | $159.75 | $121.77 |

| 72 | $172.96 | $132.24 |

| 73 | $185.36 | $142.28 |

| 74 | $196.92 | $151.50 |

| 75 | $206.83 | $159.75 |

| 76 | $241.89 | $183.13 |

| 77 | $275.61 | $205.18 |

| 78 | $307.95 | $225.81 |

| 79 | $338.93 | $245.07 |

| 80 | $368.66 | $262.13 |

| 81 | $378.78 | $268.08 |

| 82 | $389.57 | $274.49 |

| 83 | $431.23 | $283.48 |

| 84 | $451.90 | $290.49 |

| 85 | $472.73 | $297.59 |

$20000 AIG Monthly Rate Chart

| Age | Male | Female |

|---|---|---|

| 50 | $101.85 | $73.93 |

| 51 | $103.45 | $79.33 |

| 52 | $108.75 | $83.93 |

| 53 | $114.96 | $88.14 |

| 54 | $120.36 | $91.94 |

| 55 | $125.17 | $95.34 |

| 56 | $128.77 | $99.15 |

| 57 | $131.97 | $102.15 |

| 58 | $134.77 | $105.15 |

| 59 | $136.78 | $107.95 |

| 60 | $138.18 | $110.15 |

| 61 | $148.39 | $116.76 |

| 62 | $157.99 | $122.76 |

| 63 | $167.20 | $127.97 |

| 64 | $176.01 | $131.97 |

| 65 | $184.61 | $135.37 |

| 66 | $192.22 | $142.38 |

| 67 | $198.83 | $148.19 |

| 68 | $205.03 | $153.59 |

| 69 | $210.43 | $158.79 |

| 70 | $215.24 | $163.60 |

| 71 | $234.85 | $179.61 |

| 72 | $254.07 | $194.82 |

| 73 | $272.08 | $209.43 |

| 74 | $288.90 | $222.84 |

| 75 | $303.31 | $234.85 |

| 76 | $354.35 | $268.88 |

| 77 | $403.39 | $300.91 |

| 78 | $450.43 | $330.93 |

| 79 | $495.46 | $358.95 |

| 80 | $538.70 | $383.77 |

| 81 | $553.79 | $392.76 |

| 82 | $569.87 | $402.46 |

| 83 | $631.29 | $415.92 |

| 84 | $661.90 | $426.51 |

| 85 | $692.70 | $437.18 |

$25000 AIG Monthly Rate Chart

| Age | Male | Female |

|---|---|---|

| 50 | $126.81 | $91.91 |

| 51 | $128.81 | $98.66 |

| 52 | $135.44 | $104.42 |

| 53 | $143.20 | $109.67 |

| 54 | $149.95 | $114.42 |

| 55 | $155.96 | $118.68 |

| 56 | $160.46 | $123.43 |

| 57 | $164.46 | $127.19 |

| 58 | $167.97 | $130.94 |

| 59 | $170.47 | $134.44 |

| 60 | $172.22 | $137.19 |

| 61 | $184.98 | $145.45 |

| 62 | $196.99 | $152.96 |

| 63 | $208.50 | $159.46 |

| 64 | $219.51 | $164.46 |

| 65 | $230.27 | $168.72 |

| 66 | $239.78 | $177.48 |

| 67 | $248.03 | $184.73 |

| 68 | $255.79 | $191.49 |

| 69 | $262.54 | $197.99 |

| 70 | $268.55 | $204.00 |

| 71 | $293.07 | $224.01 |

| 72 | $317.09 | $243.03 |

| 73 | $339.60 | $261.29 |

| 74 | $360.62 | $278.06 |

| 75 | $378.64 | $293.07 |

| 76 | $442.44 | $335.60 |

| 77 | $503.74 | $375.63 |

| 78 | $562.53 | $413.16 |

| 79 | $618.83 | $448.19 |

| 80 | $672.87 | $479.22 |

| 81 | $691.74 | $490.45 |

| 82 | $711.84 | $502.57 |

| 83 | $788.61 | $519.39 |

| 84 | $826.87 | $532.63 |

| 85 | $865.38 | $545.98 |

Last Point on Premiums

Term insurance is usually available from 18 to 75 years old, and whole life insurance is available from 0 to 90 years old.

So if you didn’t see your sibling’s age, no worries, just contact us, and we’ll run a quote for you.

How To Buy Life Insurance For Siblings

Now let’s talk about some of the most common ways to purchase life insurance for someone else.

Through Junk Mail or TV Ads

Ever gotten junk mail from Colonial Penn, Trustage Life, AARP, or Globe Life Insurance? Odds are your mailbox is full to the top every week with junk mail from these companies!

Here’s the bottom line.

Junk mail and TV life insurance companies are some of the WORST to do business with.

While their products look professional and are offered by well-known companies, upon further examination (aka the fine print), one discovers how BAD the coverage truly is!

How Do These Junk Policies Work?

Companies like AARP, Colonial Penn, and Trustage all play the “no questions asked” life insurance game. However, coverage doesn’t cover natural death until two years have passed.

While those plans are a solution for some, the problem is that everyone, even people in GOOD health, ends up with a”2-year waiting period.”

Globe Life, AARP, and Trustage also offer term life insurance.

But the problem is that (a) these plans may cancel at 80, and (b), the premiums are designed for rate increases approximately every five years!

That’s bad because:

(a) you may need term life insurance on your sibling past 80 years old, and (b) at my company, we LOCK in the premium for the entire term, meaning NO frustrating price increases every five years!

Now let’s switch gears and discuss WHO can get the best life insurance quote for your sibling.

Beware of Captive Insurance Agents

A captive agent works for one company ONLY. Unlike us at Buy Life Insurance For Burial, captive agents do NOT have access to life insurance options.

They have one product and one product only—no custom-tailored policies and no guarantee that their product is the best use of your resources.

Work With an Independent Agent

Want the highest odds for the best coverage? Work with an independent agent!

Independent agents do the legwork for you. They shop the major life insurance companies to see which agency can offer the best value coverage for your sibling.

In turn, you’ll receive the best chance of maximizing your coverage on your sibling at the most competitive price. When YOU win, we win!

Final Steps

Ready to get life insurance on your sibling? Here’s what to do next.

If you’re interested in qualifying for a life insurance program for your siblings, there are a couple of things you’ve got to do.

- Call me at 888-626-0439

- Or click here and send me a message.

We need to establish your budget, goals, and what you want to accomplish. I also need an idea of what your sibling’s health is like so we can determine what they could qualify for and at what price.

It’s best to talk to your sibling first. Let them know what you’re thinking and get their input on the matter. It may be a difficult conversation, but you MUST talk to your sibling. At the end of the day, you’re doing this because you care.

Once you’ve gained your sibling’s consent, I’ll need to talk to them to complete the application. But we can easily set you up as the payor if that’s what you want to do.

Feel free to leave me a message if you don’t reach me because I’m usually busy talking to people, so I can’t always answer. You can also leave a comment below.

I look forward to talking to you. Take care!