9 Steps to Get Life Insurance For Adult Children

Most likely, you’re here because you’re concerned about getting life insurance for your adult children.

Understandably, if something were to happen, you wouldn’t want them to leave behind final expenses that you, their spouse, or their children would be responsible for.

That’s why in today’s article, I promise to help you understand how to secure quality life insurance coverage for your son or daughter in the following nine-step process.

The Topics We’ll Discuss Are As Follows:

- Motive

- Consent

- Goals

- Broker

- Best Policy

- Exam

- Beneficiary

- Plan B

- Waiting Period

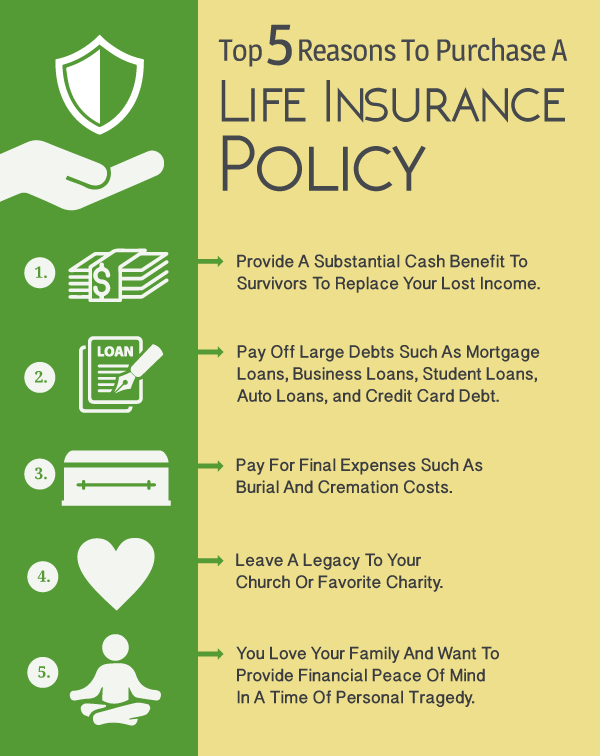

1) Establish Why Life Insurance Is Important

If you’re looking for life insurance for a grown child, you first need to determine WHY you want life insurance coverage.

Let’s look at a few of the reasons below!

Taking care of final expenses

Maybe you’re concerned about your child’s safety, or you’re worried that should the worst happen, they could leave behind financial costs that would be you or your grandchildren’s responsibility to bear.

Securing a life insurance plan is the simplest way to solve these worries. Life insurance will alleviate any debts that may result from your child passing away.

Family left behind

Another concern could be your grandchildren. Would they face financial difficulties if their mother or father suddenly passed away with no warning?

Not only would a life insurance policy cover final expenses, but it would also ensure your grandkid’s financial welfare is taken care of.

2) Gain Consent

HIPAA rules state that your child’s consent is necessary to access their medical records. As such, you will not be able to take out a life insurance policy on your adult children without their consent.

Why?

According to HIPPA rules, adults have protection over the privacy of their health information.

However, as the parent, you can be the payer, or owner, of the policy (with your child’s consent).

This means you can determine who the beneficiary is and what the details of the policy are.

Your Child’s Permission Is Required

Before you attempt to take out a life insurance policy on somebody else, you should always have a discussion with them first.

As an agent who has worked in the insurance business for many years, I have witnessed situations where the child got spooked by the parent trying to insure them without their permission.

Understandably, the child may see this as highly suspicious, even if your intentions are good.

So talk with them first. Explain what you’d like to accomplish and the reasons why you want to get insurance coverage for them.

3) Quantify Your Goals

Now, the next step in this process is to clarify the amount of coverage necessary based on why you want to purchase life insurance for your son or daughter.

Let me give you an example of this.

Given that the cost of living (and dying) continues to go up, it’s worth considering taking out more coverage than you think you’ll need.

Many parents opt for an amount between $10,000 – $25,000.

If your goal is to take care of final expenses, Buy Life Insurance for Burial can help!

- We work with the most competitive burial final expense insurance companies.

- We can give you a fair quote for life insurance coverage to help you accomplish the goals you have in mind.

If your goal is income replacement, it’s best to have a policy ten times greater than your annual income:

- If your son or daughter makes $30,000 a year, a $300,000 life insurance plan will take care of most debts and obligations.

If that’s out of range financially, you can always opt for a smaller plan. Any amount of coverage can make a dramatic difference in the lives of the people you love.

4) Find A Broker

Finding a good broker is extremely important.

A broker has access to various life insurance companies, so you can shop around and find the best one in terms of price and coverage.

A captive agent, on the other hand, does not.

A captive agent only works with ONE life insurance company, which means:

- Limited coverage options

- Limited flexibility regarding health issues

- Limited price options

It’s no surprise that some life insurance companies are strict about specific health ailments and lifestyle choices.

But unfortunately, this means that your rates could be astronomically high (entirely outside your budget).

It also means that your child might not qualify.

Again, more reason to work with an insurance broker like us here at Buy Life Insurance For Burial. We shop the major companies to help you find the best quality of coverage.

5) Select The Policy With The Best Underwriting Outcome Potential

As we mentioned above, brokers have access to multiple insurance products and companies, meaning they can help you find a quality plan that matches your budget.

However, brokers can also talk with the underwriters to establish who will offer the best product based on your adult child’s health.

Working With A Broker = Best Coverage For The Best Price

Once we have your son or daughter’s information, we’ll compare the top three companies that offer quality coverage within your budget.

We’ll then explain the benefits and drawbacks of each of these plans so you can make a well-informed decision.

6) Decide Whether Or Not To Take An Exam

Ultimately, the decision is up to your child.

Exams provide an up-to-date evaluation of your child’s health and require the following:

- Blood withdrawal

- Blood pressure check

- General questionnaire

Exams complicate matters

Should your adult child complete an exam? An exam can add an extra layer of complexity to the application process.

Bypassing the exam makes sense if the life insurance policy is under $500,000 in coverage.

At that amount, an exam is unlikely to lower your premium by much more than $5.00 or $10.00.

The more significant issue seems to be getting an adult child to complete an exam, especially if they’re out of state.

Get Life Insurance With No Exam

That’s why I would recommend looking at a non-medical application when the exam isn’t necessary.

The good news is if you’re looking for a final expense life insurance plan, most of those plans do not require an exam.

However, they’ll likely require your child’s signature to authorize the application, and they may also need a phone interview.

7) Carefully Determine The Beneficiary Arrangement

Since you’re probably going to be paying for the policy, it makes sense to nominate yourself as the beneficiary.

However, you may want to name someone else as a beneficiary as well.

I always recommend my clients do the following:

- Review your life insurance policy every year or so.

- Keep any information regarding your chosen beneficiaries up-to-date.

You wouldn’t want your child’s ex to receive a substantial amount of money intended for your grandchildren, would you?

8) Create A “Plan B” In Case Your Grown Child Is Declined, Rated Up, Or Cannot Find Sufficient Coverage

If your child has:

- Health problems,

- A criminal record,

- Misdemeanors, or,

- Traffic issues,

You may run into issues getting their application approved.

Think about the worst-case scenario and get a backup plan in place. Some coverage is better than no coverage.

Again, we can help you design a back-up plan =).

9) Await The Decision

If you apply for a final expense life insurance plan for your adult child, you’ll probably receive a decision within a couple of days.

However, if you opt for a non-medical life insurance plan to replace income, it’s going to take somewhere between several days to several weeks.

Either way, be patient. Odds are you will get a positive result and gain peace of mind knowing your child is covered.

Summary

My twin girls Emily and Eva, thank you for reading! And we genuinely hope you’ve gained valuable information on your search for life or burial insurance.

If you’re ready to discover your options for life or burial insurance, call me at 888-626-0439 now for your free life insurance quote!