Guaranteed Universal Life Insurance For Seniors: Rates & “Fine Print” Revealed

Did you recently receive a quote for a guaranteed universal life insurance policy on a senior from an insurance agent? Would you like to make sure it’s the best deal possible?

Whether you’re looking for guaranteed universal life insurance for yourself or a senior loved one like your parent, you’re in the right place!

My goal is to help you determine if guaranteed universal life insurance is the right choice for YOU.

I promise that by the end of this article, you’ll understand the following:

- How guaranteed universal life insurance coverage works

- Who it suits (and who it doesn’t)

- How to qualify

- Your alternatives

So, let’s begin!

NOTE: Would you prefer to watch a video instead? Check out the video below. Enjoy!

Quick Navigation Article Links

The Basics Of Guaranteed Universal Life Insurance For Seniors

When I write articles on term life insurance or life insurance to cover burial costs, I like to start with the basics.

With that said, here’s how guaranteed universal life insurance programs work:

Guaranteed universal life insurance (also known as “no-lapse universal life insurance” or “GUL”) pays money to a named beneficiary regardless of when the insured dies.

Unlike most universal life insurance plans, guaranteed universal life insurance policies carry a no-cost “premium guarantee rider” that fixes premium rates, so they never go up.

In other words, as long as you pay the premium ON TIME, your policy will NEVER increase. Nice, right?

And with GUL plans for seniors designed to last until age 121, they provide lifetime permanent protection.

But WAIT!

Not ALL universal life insurance policies are the same.

That’s why it’s crucial to understand how universal life insurance for seniors has changed over time.

Universal Life Insurance Policies in the 80s and 90s

In 2018, the Wall Street Journal and Forbes reported that seniors were losing their universal life insurance policies in huge numbers because of how agents improperly designed them.

In the past, clients could adjust premium rates if they ran into financial difficulties. Plus, agents could custom-tailor universal plans more easily to fit the client’s needs better.

However, the resulting policies ended up being overly-optimistic, promising things that never panned out.

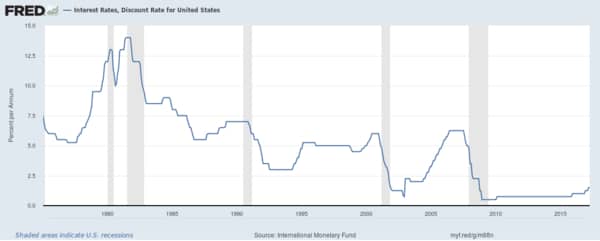

In fact, one of the most significant issues with older universal life insurance plans was the assumption that interest rates would remain continuously high.

Monthly US Interest Rates Since 1975

Why is this a problem?

Because interest rates directly impact the sustainability of the client’s insurance policy.

And unfortunately, insurance companies allowed agents to assume that interest rates would remain high and NEVER change.

Of course, on paper, this looked great! But here’s the problem:

Nobody can predict interest rates with perfect accuracy.

Surprisingly few people can accurately forecast where interest rates will be 5,10 years from now.

And, surprise, surprise, interest rates plummeted…

Over the past several decades, we’ve experienced historically-low interest rates.

As a result, any policies based on interest rates that were WAY higher than reality experienced dramatic premium increases.

We’re talking about premiums going up by 200%, year-over-year, mostly for fixed-income seniors.

So, let’s fast forward to today!

I’ve been in this business since 2011. I’ve seen countless seniors struggle with these older policies.

And of course, many of them feel deceived. Wouldn’t you if your insurance rates suddenly doubled?!

But don’t lose hope just yet.

The good news is that guaranteed universal life (GUL) insurance policies available to seniors NOW are MUCH safer than those sold in the past.

How Our GUL Insurance Policies for Seniors Compare

Premium guarantees

These “no-lapse” guarantees prevent premium increases, making the policy more palatable to many consumers.

Cannot cancel due to age or health

GUL insurance plans designed for seniors usually guarantee lifetime protection, assuming that you pay the premium on time.

More coverage for less money!

Plus, you may qualify for more coverage per premium dollar compared to policies such as whole life.

If you want to maximize your beneficiary’s payout, then looking at a GUL policy is a smart decision!

Why Seniors Own Guaranteed Universal Life Insurance?

Final Expense Protection

Do you want life insurance that covers your funeral expenses? Yes? Then, a guaranteed universal life insurance product may be the answer.

Take a look at this scenario!

A 70-year-old couple in South Carolina wants $25,000 in life insurance coverage to cover their burial expenses and clear up any remaining debt.

So, what did they do? They went with a GUL insurance policy.

Not only do they receive full coverage from day one, but they also pay almost HALF of what a standard “burial insurance” policy would cost!

Even better, my clients CANNOT outlive their coverage and will never experience premium increases (as long as they pay on time).

Replacing Your Income

When a loved one dies, there’s no guarantee that their partner will receive their spouse’s pension. This can have devastating financial consequences.

Many times the motivation to purchase life insurance stems from the non-transferability of pension schemes.

So, what should you do to replace the lost income? Opt for a guaranteed universal life insurance plan!

Unlike term insurance, you’ll never have to worry about outliving your life insurance coverage.

Plus, GUL insurance arguably provides the best source of maxed-out death benefit a permanent policy can provide.

Leaving Money Behind

Perhaps, your goal is to leave a substantial amount of money behind to a loved one, a close friend, or even a school or church.

If so, guaranteed universal life plans are perfect for seniors looking to do just that.

Possible Issues With Guaranteed Universal Life Insurance For Seniors

Right, now it’s time to discuss how to qualify and address some of the possible roadblocks you might experience.

High Minimum Coverage

First, the minimum coverage for a guaranteed universal life insurance policy is $25,000.

If you’re 100% certain you want less than this, check out getting a whole life burial insurance plan instead.

Minimum coverage amounts for whole life burial insurance start at $1000, perfect for funding a cremation or funeral.

In-Depth Underwriting

Compared to other products, it may be more difficult to qualify for guaranteed universal life insurance coverage as a senior.

In truth, you must be in GOOD health. Luckily, checking to see if you qualify doesn’t cost you anything.

If you want to find out if you can qualify, please ring me at 888-626-0439 or message me here.

Buy Life Insurance For Burial works with MORE than one insurance company so that we can find you the best deal possible.

No Exam Necessary [Most Likely]

And one final bit of good news – most guaranteed universal life insurance plans do NOT require an exam or a physical (unless you’re applying for a VERY large policy).

Thankfully, most insurers only need to look at your medical records for smaller policies.

Guaranteed Universal Life Insurance For Seniors Rates

Now, it’s time to check out the rates!

Below, you’re looking at a $50,000, no-lapse universal life plan for a non-smoking 65-year-old male:

For $50,000 in coverage, coverage costs approximately $120 to $150 for standard or preferred underwriting.

Keep in mind that rates may be higher for you.

Guaranteed Universal Life Insurance Versus Burial Insurance

For argument’s sake, let’s say you’re in fantastic health and can secure the rate above.

I think it’s still a good idea to compare how a guaranteed universal life insurance policy stacks up against a whole life plan.

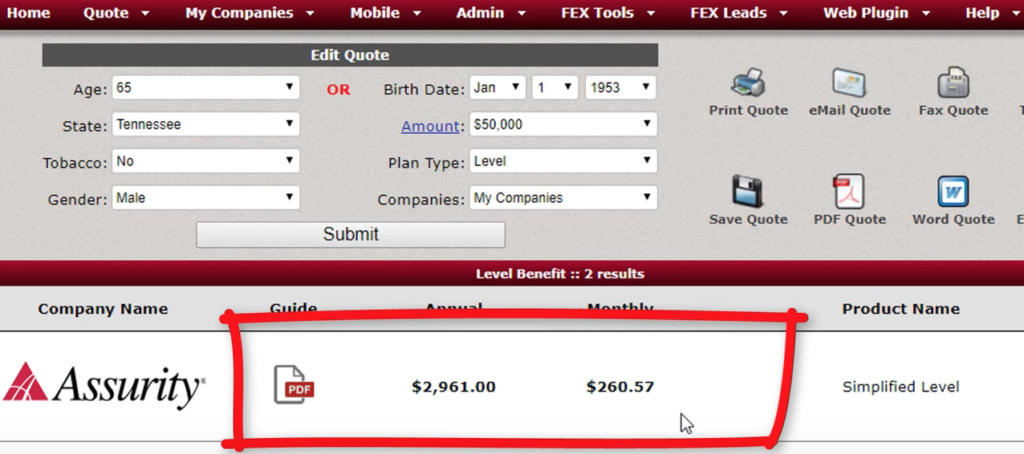

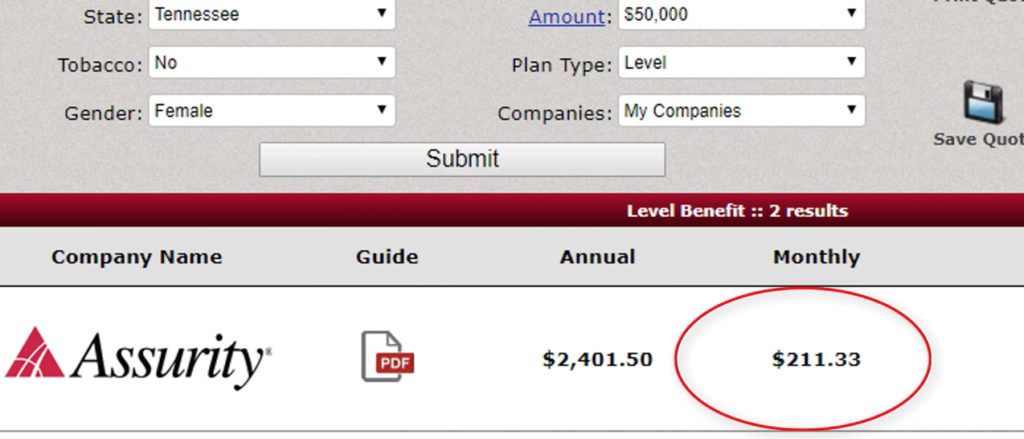

Check out how an Assurity $50,000 burial insurance plan compares below!

A monthly payment of $260.57! This is one of the most competitive $50,000 burial insurance plans I know of. There’s a whopping $110 price difference!

That’s A LOT of money!

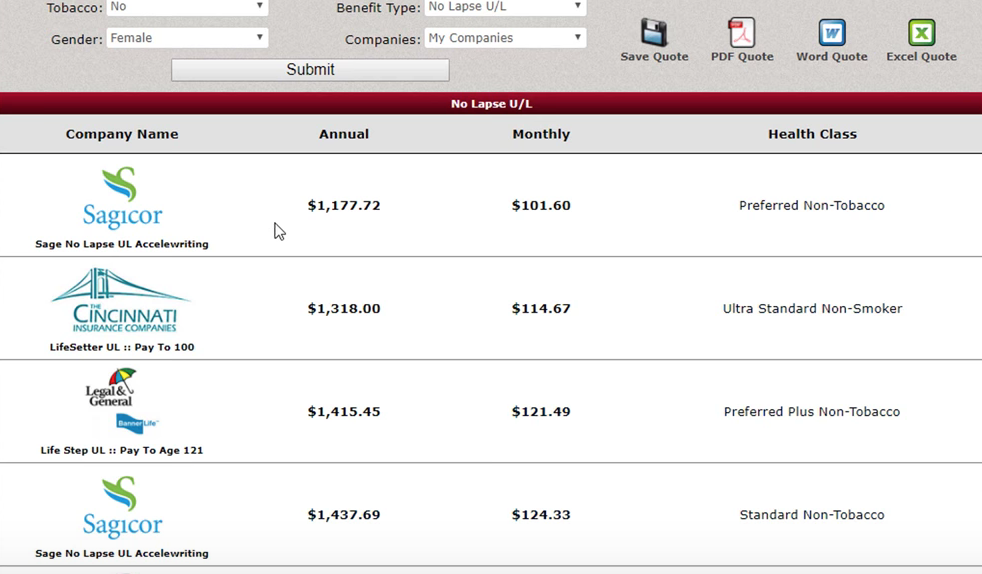

Let’s also look at a $50,000, no-lapse universal life insurance plan for a female 65-year-old non-smoker.

Premiums are around $100 to $125, depending on which program you qualify for.

Now, let’s compare the GUL insurance policy rates above to a whole life plan:

$211 per month for $50,000 in burial insurance cover! That’s almost DOUBLE the price for the SAME amount of life insurance! Wow!

Wrapping Up Why I LOVE GULs Insurance For Seniors

So, let’s recap the benefits of Guaranteed Universal Life Insurance for seniors:!

- Lifetime protection,

- A “premium lock” that prevents frustrating premium increases,

- More coverage per premium dollar.

Can you see why I LOVE this insurance product?

Of course, you can. Plus, I think a GUL insurance policy is PERFECT for seniors who fit the following criteria:

- In good health

- Want as much death benefit coverage as possible

- Need a plan to pay off a mortgage, replace lost income, leave money behind, or cover final expenses

Thankfully, it doesn’t take long to get qualified, either. Usually, we can get approval within several days or several weeks.

Naturally, it depends on how much information the insurance company needs, which can differ between companies.

How To Get More Information On A Guaranteed Universal Life Insurance Program For Seniors

First, find an agent – someone you want to work with. Of course, I nominate myself. I can’t help it. I love what I do, and I want to help =)

All that’s needed is a quick phone interview. I’ll ask you some health questions and discuss YOUR goals. Then within 10 minutes, I can give you an accurate estimation as to what premium you’ll potentially qualify for.

My goofball son and I thank you for reading and truly hope you enjoyed today’s article.

If you would like to discover your life or burial insurance options, call me at 888-626-0439 now for your free life insurance quote!

To get started, click here to send me a quote request! Or you can call my team and I at 888 626 0439.

If you don’t reach us, leave a voicemail. We’ll get back to you ASAP!

Thanks again!