Gerber Life Insurance Review [Rates, Secrets Revealed]

Looking for a quote for life insurance or burial insurance? Click here and send me a message with details of what you’re wanting to accomplish. If you’d prefer to talk live, call 888-626-0439 to speak with me directly.

Today’s Topic Is Gerber Life Insurance Review [Rates & Secrets Revealed]

NOTE: Would you prefer me to present this information to you in video format? Watch the video below for the complete presentation. Enjoy!

Here’s An Overview Of Today’s Topic:

- About Gerber Life Insurance

- What Gerber Life Offers

- What Person Is Best Suited For Each Product

- Case Study Examples

- Stories From The Field

- Alternatives To Gerber Life Burial Insurance

- Top 7 Reasons People Buy Term Insurance

- Final Thoughts

- Next Steps

About Gerber Life insurance

Gerber Life Insurance is a rather well-known company. They offer life insurance and burial insurance products to people of all ages, not just children, not just adults, but also everything in between.

They’re most notable for the Gerber Foods logo that you see in its advertising. I’m assuming you’ve got a pretty basic understanding of Gerber life insurance. That’s why you’re getting a product review. I won’t spend too much time describing them, but let’s just jump in, to really what they do and what they have to offer so that we can help you out the best.

Gerber really offers three particular types of life insurance products. First is term life insurance for adults. Second is guaranteed acceptance, life insurance for adults. And the third is whole life insurance for adults.

What we’re going to do is take a look at each. We actually take you to their website and walk through the application process, look through the fine print, and discuss the pros and cons of each.

We work hard to help individuals get affordable life insurance, regardless of their age and health. We search out the most competitive prices and best value coverage to pass on the savings to you.

Let us help by providing a free quote. Simply call (888) 626-0439. You can also submit a message to the left-hand side of the screen and we will reach out to you within the next 24 business hours.

What Gerber Life offers

First of all, we’re going to start with the Gerber term life insurance.

The basic way to understand term insurance is that it is a terminating life insurance. What does that mean? It means that it lasts up to a particular point in time before cancelling. And what that means simply is that yes, you get coverage, but if you outlive the end point, you lose the coverage.

What I want to do is really, instead of you taking my word for it, I want to actually take you to their website and show you a collection of images and web pages where you can see this for yourself as long as analyzing, their particular rates.

We’re here at https://www.gerberlife.com/adult-life-insurance/term-life-insurance. We’re here on the web page and again this is really just a walk through of how the product works and we’re just going to scroll through here.

You can see that they have covered options from 25 and 100, $50,000 premium is locked in for the policies duration available between 18 and 50 with no medical exam for up to $100,000 in coverage and they’ve got different lengths of time in which the term insurance lasts.

Let’s keep going here. Just going to read through this, describes how term insurance works, tells you what happens at the end of the term insurance.

Just so you understand, you can choose to end the policy agreement or renew your policy. Sometimes you can renew it, sometimes you can’t. It just depends on the length of time and how old you are.

They’ve got even a customer service complaints here, but let’s go ahead and focus on actually reviewing to get a free quote. What we’re going to do here, if you’ll just bear with me, I’m going to put in since most people here are going to be in the 50 and older ages, sixty year old male, non-smoker and I’m going to put in a fake email and then we’re just going to look at some options.

Here we have the length of time and the prices for coverage. I’m going to take you through each of these 10 year term. You can see what we have here for the costs and this is just assuming you can be approved.

This was the 15 year term and this is the 20 year term and this is for sixty year old will compare this to what you could get a if you were to buy a plan outside of Gerber in a moment, but let’s say we want to start with a 10 year term $100,000 plan. Let’s click apply now.

Now what this application process does is actually really neat to do it all over the phone or all over the Internet. You may have to do phone interviews. Sometimes we’ll follow up with you. This information here, if you’re wondering, is the MIB medical information bureau release. You can read through this in your own time.

What it basically is doing ,and say it’s going to pull your medical information from the MIB, which is a membership organization that helps determine insurability a standard practice with all insurance carriers.

See what you do is you just fill this application out and then here’s the actual health questions for the term insurance product, so we see, of course we see term insurance here below here.

We have a five year look-back on felonies, a driver’s license suspended or revoked for two years, more moving violations five year, look back on health consultation and hospitalization, five year look back on alcohol or drug use issues. Ten year look backs on major health issues and this is just existing coverage.

Now, what this does, just you understand, is that this particular plan is going to, essentially just apply. You may get a higher price just because you answered yes to one of these questions, may not necessarily mean you’re not going to get coverage, but it’s just a starting point.

There’s usually different rates available, like what you’ve shown here is a particular rate. It may be higher priced, comes back at a higher price. It just depends on Gerber’s underwriting. I don’t have that much information, but I can tell you that there are circumstances where this may answer yes, but will be higher-priced may decline you. It just depends on what the underwriters say.

Benefits, exclusions, and limitations. This is important to understand. No medical exam is necessary. In most cases, coverage is dependent on answers to health questions and a physical may be necessary for cause and for applicant’s age, 50 or older to apply for more than 100,000.

What this is saying here is that if you’re going to apply for 100,000 dollars or more and you are over the age of 51 or 51 or older, you might have to do an exam and we’ll get into later. If you don’t like being stuck with needles and peeing in a cup, you can actually get coverage for much more than a hundred thousand without an exam with many insurance companies.

That’s the overview of Gerber’s term life insurance product. As you can see, you have 10, 15, and 20 year options. You may have the ability for 30 year at certain ages. Most of the time it’s going to be 10 through 20 and you can see what rates there are. Now, keep that in mind.

We’re going to look at some rates for other companies momentarily, but I want you to be aware of bottom line and term insurance will only last for that period of time. The premiums remain the same, but you do have the capability potentially of outliving the coverage and not having the term insurance at all or paying more you don’t necessarily have to pay.

And we’ll talk about that later.

If you like what you’ve read so far and are interested in seeing what you may qualify for call us at (888) 626-0439 for a no obligation quote from an expert in the field.You can also request a quote by using the message box found on this page. We will get in touch with you within 24 business hours with more information.

OK, so let’s talk about guarantee. A Gerber’s life insurance is guaranteed acceptance whole life insurance. This is their permanent product. Maybe you don’t like a plan that would cancel. Maybe you want one that doesn’t cancel it a later date. That’s what this particular guaranteed acceptance whole life insurance plan does.

At Gerber, the rates never increase and the plans cannot be canceled due to age, but these plans do not provide first day full coverage based on your health, which means if something happens within the first two years, you’re not fully protected, only your money that you paid in plus interest is paid back to your beneficiary.

Let’s again take a look at the website so you can see this for yourself. OK? We’re here as you can see, the guaranteed life insurance page. Let’s go ahead and just scroll through here and read this.

Guaranteed life insurance plans help provide for costly final expenses. Your acceptance is guaranteed. No medical exams are required. No health history issues are an issue. You can get between five to 25,000 in coverage. It does have cash value. Scrolling down through here, frequently asked questions.

Guaranteed life insurance is available for adults between 50 and 80, 5 to 25,000 in coverage. And then let’s click here because there’s a little bit more we got to know about this conference room.

Click on view all guaranteed life insurance questions. We’re gonna look through here. Some of this we’ve already answered.

The next thing I’ll help you through is the so-called ‘smoking gun’. The Gerber life Guaranteed life insurance policy comes with a graded death benefit limitation.

It applies to the first two years of coverage when the policy’s issued. If death occurs within the first two policy years for any reason other than accident, all premiums plus 10 percent interest shall be paid to the beneficiary.

If death is due to accidental causes within the first two years. The full death benefit shall be paid to the beneficiary. After the two-year graded period if the insured dies for any reason, the full face amount of the policy shall be paid to the beneficiary. If the insured dies by suicide within two years from the issue date, the amount payable will be the premiums paid for the policy plus 10 percent less any debt against the policy.

What does this mean? We just spell it out to you.

As I mentioned earlier, what this is saying, is that if you die from natural causes, if death occurs within the first few years for any reason other than an accident. That just means if it’s not an accident, all premiums plus 10 percent interest shall be paid to the beneficiary. That means there is a limitation of coverage for two years if you buy one of these plans.

It doesn’t matter if you’re in good shape. It doesn’t matter if you’re in bad shape, If you apply for a Gerber graded death benefit limitation plan or guaranteed life insurance plan, it’s a two year waiting period product no matter what.

Now let’s go back and run some quotes. Again, I’m just going to show you a 60 year old male with a fake email to get the quote. This is what you’re looking at for $10,000 in coverage: 63, 89 and we’ll compare that to some prices again momentarily.

Now, Gerber also offers a whole life insurance plan that does not cancel at a later date where the rates never increase, it can’t cancel due to age or health. And if approved, will provide first day full coverage based on health.

Again, let’s look at some permanent coverage options so you can see how their prices would compare. We’re looking at again, the 60 year old male, non-smoker, 25,000 in coverage rates all the way up to a hundred 50,000, $131 and fifty cents a month to concede the other premiums as well. We’ll just scroll through here like we have been talking about the plan. You can get $25.000 to $150.000 in coverage.

No medical exam is necessary for adults up to age 50 and coverage up to 100,000. If you go over 100,000, you may need to have an exam. Adults 18 to 70 can apply. And then let’s just click on the free quote while we already did that.

Let’s go ahead and actually, let’s do the free quote and then see if we can get some health questions. Usually this is the same series of health questions with these companies.

Remember earlier we talked about the term insurance plans. These are identical questions that they’re asking here. OK, so take a look at them. Same exclusions. Limitations.

Really it’s just they switched term with whole life. Of course it’s going to be a higher price with whole than it does with term insurance. Now I have to ask a question: Why would people buy certain Gerber life insurance products under certain circumstances?

What person is best suited for each product

Let me describe who is each type of policy right for. The person who buys the term pro term insurance product needs to be price conscientious. Usually they buy that because they see the guaranteed or the whole life insurance products and they just balk at the price and they feel like, well I’ll just substitute it, but something’s better than nothing. Let me get a term insurance product at least so I can have some kind of coverage on the book.

Maybe they want more than just the typical $10,000 plan or even $25,000 plan. They feel like they’ve got an obligation higher than that. That needs more coverage. They feel the necessity to buy more term insurance because of that.

Then people buy guaranteed acceptance whole life insurance because they’re just in really bad health. They’re not going to qualify for the regular term or the regular whole life insurance product. And this is their last ditch effort and they just feel like based on the fact that they can’t qualify for those other products, that this is better than nothing, let’s just apply for that.

People buy or apply for the whole life insurance because they want permanent protection, they feel it’s important to not outlive the coverage like term insurance. They’ll pay the higher price for that peace of mind.

Case study examples

High Blood Pressure Coverage

A young couple contacted us after the birth of their first child. They were overwhelmed by a sense of love and a need to protect this new addition to their family and new that one of the best ways to do that would be to take out two life insurance policies to ensure their little one would be taken care of if anything happened to either of them.

The only issue was that the wife had high blood pressure. She had been through a particularly difficult pregnancy with her hypertension and had started taking medication to regulate her blood pressure levels.

I looked at a number of options for this couple and was able to provide them with a free quote for first day coverage at a premium price.

Though I can’t guarantee the same outcome for every couple, we here at Buy Life Insurance for Burial work hard to provide affordable coverage to clients that gives them peace of mind in meeting their goals.

Primary Income Coverage for Mortgage

A young man recently contacted us after he and his wife had purchased their first home. Because he was the primary breadwinner, they were concerned about what would happen if he passed away unexpectedly and his wife had to continue to make mortgage payments.

This client was concerned about the underwriting process due to a history of depression. He was taking anti-depressants and had been on this prescription for a number of years.

He was relieved to discover we were able to get him first day full coverage at a price he could afford. Though we can’t guarantee the same outcome for every client, we do our best to provide the best opportunity to get quality coverage in place by looking at a number of options among a number of providers.

Stories from the field

My work in the life insurance business has allowed me to meet a lot of wonderful people who are being taken advantage of by overpriced life insurance plans. I met one such couple back in 2015.

This couple had been paying on a life insurance policy for a couple of months when they got in touch with me. I stopped by their house after receiving a request from them and we struck up a conversation about different life insurance options.

As we talked they shared that they felt uncertain about requesting information because they felt leary of salespeople. I could sympathize with their feelings and explained I would simply explain their options to them and allow them to make the final decision without any pressure on my part.

The husband who had been the one to request more information told me he was satisfied with the plan they had, but was curious what our rates would be.

I was honest with the couple and told them the coverage they had was inadequate, as it was overpriced and costing them more than it should.

As I spoke I noticed the wife hanging on every word, while the husband did not seem convinced. Unfortunately the wife remained silent as I finished explaining different options and collected my things to go.

As I walked to my car I felt pretty disapointed in my ability to convince this couple that we could save them money every month. It was clear in my mind that they could get much better coverage at a much better price, but somehow I had failed to communicate this to them.

As I began to put the car in reverse, I noticed the garage door open in front of me and the husband rushed out to my car.

He appologized and explained that he shouldn’t have sent me away so quickly. That he simply felt confused about everything and wondered if I would be willing to come back inside and explain everything again.

I happily obliged and was able to get this couple switched over to a much better plan that saved them $400 a year in premium payments.

Alternatives to Gerber Life burial insurance

Now let’s move on to alternatives to Gerber life insurance products. Look, they’re not the only life insurance product to offer coverage to seniors or anybody at any age. And it’s always good to have a second opinion if you’ve ever had any health issues and you’ve wondered if the opinion of the doctor is the only option available, you want to get a second opinion. The same idea or mentality applies to buying life insurance.

There’s no negativity to knowing your alternatives. It just gives you more options. And usually more options means a better deal. Buying permanent life insurance through a broker or an independent agent (much less term insurance – we’ll get to that momentarily), but buying permanent insurance.

That would be the whole life insurance and guaranteed acceptance insurance, I believe it’s best bought through a broker. I’m a broker. I’m an independent agent. I represent a variety of different companies so I can shop to see who’s going to give you the best price.

What I’m going to do here is just do a quick comparison for a 60 year old male, non-smoker and a female, both for that matter, so you can compare some prices to not just their whole life insurance product, but also they’re guaranteed acceptance plan and just show you how you really could save some money. Assuming you could qualify for these plans and get more coverage for the kind of premium you’re comfortable paying.

Let me take you back over to these screens. I’m going to show you Gerber’s prices and then we’ll show you my prices and we can do a little comparison. Here we are on Gerber life insurance page.

Again, I’m showing you the $10,000 plan for $63.89 a month. This is for a sixty year old non-smoking male. Let’s take a look at what a 60 year old non-smoking male would cost for a simplified issue product that we could potentially get.

In our case, there are companies, as you can see here from the upper thirties to the mid forties and make a little higher than that, but again, compared to $63,89 versus maybe a round of mid forties, that’s a potentially $240 a year savings.

And in fact if you were to get say around 13,000 in coverage, what you’ll find is it’s still less expensive than the 10,000 and it looks like you could probably get all the way up to 15,000 for a male, non-smoker. And potentially for the same price to get 5,000 more in coverage.

That’s really important because the prices for burials continue to go up and why pay 10,000 when you could get 15 with a good company.

This comparison is meant to just draw the difference of price, but also to draw the difference in quality. 100% of the time we know that Gerber Life Insurance will make you wait two full years before you’re fully protected for the guaranteed life insurance product.

However, these products here may qualify you for first day full coverage. Even with one payment in, you’re fully protected for the $15,000 if you end up getting the same price and you want to say, pay the same price as a $10,000 guaranteed life insurance plan at Gerber that makes you wait two years.

The point here, ladies and gentlemen, it’s just to compare and contrast the difference in pricing and quality of coverage you may be able to get.

Let’s take a look real quick at a female. With the same rate, sixty year old female, and then let’s take look at 10,000. That’s $51.06 a month for a quote with Gerber life. And that’s a two year wait.

And then if we look at a female here, 60 year old non-smoking female for 15,000 (almost the same thing), you’re looking at somewhere between mid forties to lower fifties. Again, a comparison: we’re getting almost 5,000 more coverage with most of these companies for the same price and first a full coverage potential.

Again, 10,000 low upper twenties, most likely mid thirties if you just keep the 10,000 substantial savings and the potential for first day full coverage.

Pointing the takeaway here, ladies and gentlemen, is you can see there’s a big value proposition difference when you get something like this versus the other options. What about the whole life insurance?

Again, we’re looking at a 60 year old male for a whole life insurance plan that’s $250 a month. Maybe you want a lot more coverage and you want permanent coverage and you’re not afraid of paying a price at that premium. How does this compare to other options?

What I’m going to show you is what’s called a guaranteed universal life plan. It is very similar to whole life insurance plan is permanent coverage. As long as you continue to pay the premium, you can never be canceled due to age your health. And it gives you that permanent protection from the first day.

It’s comparable to what Gerber’s whole life insurance plan offers. Let’s just look at what you could get for $50,000 plan and compare. Check this out guys. This is for a male, 60 year old, 50,000. Literally you have the potential if you qualify to get as low as a $101.52 a month for a $50,000 permanent, no lapse guaranteed universal life.

Or if you’re rated up it may be $126, may be $188, but it’s substantially less than this $250 a month premiums This is just to give you an example of the amazing price difference.

Here we’re looking at a female to compare and for a $50,000 plan, sixty year old female non-smoker. It’s a $150.50 with Gerber’s whole life insurance product. And for a female you’re looking at potentially a price as low as $86,62 for $50,000 in a guaranteed universal life plan.

And yes, it may be rated up to a $105 or a $148, but it’s still less expensive than if you write it up here with Sadie core, it’s most likely that you’ll be rated up with the Gerber life product too.

And the other thing is that if you go higher than this with these plans, you don’t, let’s say you want more than a hundred thousand, you don’t have to do an examination in most circumstances up to about 250,000, maybe a little bit more.

As you can see, there’s some substantial advantages by using another company besides Gerber. Let’s take a look at also a term insurance products. Let’s take a look at some term life insurance comparison.

Same deal. We’ll just look at a $50,000 plan for sixty year old male and female, and compare that to Gerber’s and then decide on, you know, what’s the better deal? Let’s take a look.

Here I’ve got a 50,000, $62 a month premium for 6,000 coverage for a 60 year old non-smoking male for 10 year term. If we compare a 10 year term, 60 year old non-smoking male for 50,000, you literally have the ability to pay as low as $24 a month. Again, that’s compared to $62 a month for the same 10 year length of time. You might be rated up, maybe even a little higher, but it’s still substantially less expensive.

Now we’re looking at a 15 year term for $50,000 of coverage. You’re looking at $79.70 a month for male, sixty year old non- smoker. And if we look at a male, 15 year term, substantially less potentially.

Lower thirties even to mid fifties, which again, big difference from almost $80 a month. And for a 20 year term, 50,000 of coverage, we’re looking at $82 a month potentially for sixty year old male, non-smoker and in comparison we’re looking at potentially still low forties to mid seventies, substantially less expensive than $82 a month.

Let’s look at the ladies here for 50,000 and 10 year term. Sixty year old non-smoker is $42 even for a 10 year term, 60 years old, female, 50,000 in coverage. It could be as low as $18 a month and change maybe more like upper twenties to mid thirties. Again, big difference.

A 15 year term, 50,000, 48 or 9 a 15 year term for female, $25, 77 as low as it could be in the upper or mid thirties for a 20 year term with Gerber life female, sixty year old non-smoker $56 a month. And if you shop through a broker, could be as low as $29,49 a month up to the mid forties potentially.

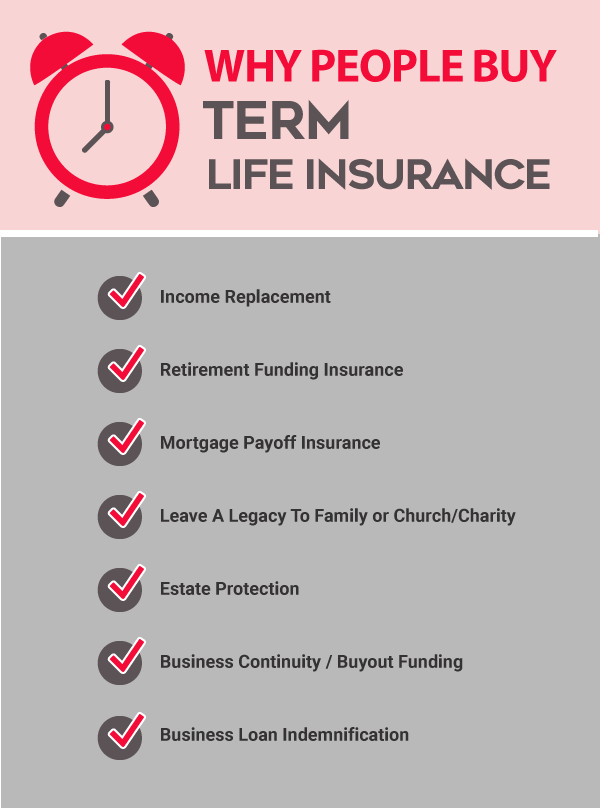

Top 7 reasons people buy term insurance

1.Term insurance is affordable

If you are on a tight budget, term insurance is an affordable option. It provides quality coverage at a much lower premium than other types of insurance.

2.Income replacement

The primary reason people buy life insurance is to make sure their loved ones are financially secure. If income replacement is a concern, term insurance does a good job of providing a lump sum payout to cover any financial obligations your loved ones may be left with.

3.Retirement funding

If you are looking to find long term funding for your retirement, a term insurance policy can help. If you pass away unexpectedly, funding to your retirement plan comes to a halt unless you have a source for continued funds.A life insurance policy can continue to fund your retirement plan to ensure your loved ones can benefit from the retirement savings.

4.Out of love

If you are concerned about what would happen to your loved ones if you passed away, term insurance can provide peace of mind. No one wants to think about their loved ones struggling financially. Term insurance can provide financial stability at a time when it is needed most so that your loved ones can continue to pay bills and maintain the lifestyle they are used to.

5.Custom length

If you have a particular time period in which you are paying off a loan, term insurance offers a flexible time period for coverage.So for example, if you have a 30 year mortgage, you can get a 30 year term insurance plan. This ensures you don’t overpay for coverage when you don’t need coverage for a longer period of time.

6.Pure insurance need

If you want a simple and straightforward insurance plan for the short term, one of the best options is term insurance. There are no added costs involved and it generally more affordable than other types of insurance.

7.Exams are optional

If you are concerned about the exam process, did you know you can get term insurance with a non-medical application that allows you to skip the exam process?Underwriters can rely on previous health records so that you don’t have to have an exam if you Life insurance has become very competitive these days and companies have come up with different ways to entice you to buy from them. One of the ways is to provide life insurance coverage without requiring an exam.

Final thoughts

As we wrap this up here, the important point to point out is I can’t promise any of the premiums and coverage options I showed you you can qualify for. I have to always say this just as a primer because some people think, oh that because it shows that it must be it. No, it’s not the case. I have to explain to people that these are just potentials for coverage.

It all comes down to your unique health situation and that should make sense to you, right? The underwriters have to look at your health, your age, whether or not you smoke and other variables to determine ultimately what they want to price your coverage at.

These are just premiums and your unique scenario just depends on your unique scenario, but the point I’m showing you these premiums is to compare and contrast the fact that by looking at other options, you may have the high potential of getting a better rate or better coverage or just an overall better deal.

That’s why I’m a big believer in shopping with a broker. You want to get the best price and coverage, whereas if you stick with one company, sure it’s maybe a good company, but it may not be the best deal for you.

Always investigate your second options and get those second opinions and if that’s something you’re interested in doing, and applying for it, the process is very simple. You got to find an agent in most circumstances.

If you liked the idea of shopping for the best overall deal, and that’s why I nominate myself and all seriousness. I’m an insurance agent. I help people across the country and I do this on a daily basis.

Thanks for reading, and I hope you’ve gained truly valuable information on your search for life or burial insurance. If you’re ready to discover your options for life or burial insurance, call me at 888-626-0439 now for your free life insurance quote!

I shop for people to get them the best price and coverage and let’s say you and I work together, our next step would be for me to listen to your goals and drop a quote that I think you may qualify for and if you accept that quote and you liked the idea of it, we’ll apply over the phone or via the Internet. Very little reason to meet personally nowadays.

And then usually after several weeks or days, depending on the kind of product that we get, your coverage is either approved or declined. I will tell you either way, if it’s approved, great.

You’ll get your policy several weeks in the mail and then that’s it. If its declined, then we’ll just look at some plan Bs or Cs. There’s always other options in most cases to pursue if the first option doesn’t work.

Next steps

What’s the next steps? If you’re interested in applying for some kind of life insurance and you want to see what your other options are besides the Gerber Life Insurance, here’s what you need to do:

Go to buy life insurance for burial.com. Request a free quote. That way you can see and compare what your options are, or you can call me at 888-626-0439 and speak with me live.

I’ll be happy to give you a free quote in about five to 10 minutes tops and then you can decide how you want to proceed from there. Please leave a voicemail if you don’t reach me. I am pretty busy talking to people all day.

Thanks for reading this article. I hope it has influenced you to look into getting life insurance coverage. If you would like to find out more about what you might qualify for, call us at 888-626-0439 or send us a message using the communication box on this page.