10 Steps I Took To Get My Parent Burial Insurance

If you’re reading this article because you want to find burial insurance for your parents, but you’re not exactly sure how to do so, don’t worry!

This article will explain how you can secure competitively priced, excellent burial insurance coverage for a senior parent.

And I’ll do this by describing step by step how I found a quality burial plan for my elderly mother. So let’s get started.

Quick Article Navigation Links

- Talk About It

- Goals and Plans

- Health Record

- Find an Agent

- Products

- Exam?

- Payment

- Beneficiary

- Application

- Review Policy

- Free Quote

Step # 1 – Have an Open Conversation with Your Parent

As a life insurance agent, I’ve helped many clients sort out quality burial insurance for their parents.

And, the first thing I’d like to say is that the biggest impediment IS the parent!

Adult children tend to avoid talking about this issue with their parents. And unfortunately, this is what you need to do first.

I’ve come across multiple cases where parents had absolutely no idea their children wanted them to apply for burial insurance.

And worse yet, some parents assume their kids were trying to profit from their passing.

Obviously, that’s not the case (for most families). And most likely, you want to secure burial insurance for your parents because you’re concerned about funeral costs escalating out of control.

But one problem with securing life insurance on someone else is this:

It’s illegal to do so without their consent.

Your parents must agree wholeheartedly to the process for you to purchase burial insurance for them.

That’s why it’s prudent to sit down with your mom or dad and have an honest conversation.

My Experience With My Mom

When I had this conversation with my mother, it was a strange experience. But as a life insurance agent myself, I’ve seen too many families struggle with the passing of a loved one without sufficient coverage or any coverage at all.

Money has a way of destroying even the best of relationships. A sudden demand for money to pay a funeral can cause otherwise stable, loving families to bicker and complain about who pays what.

Although my mom’s pretty tough, she was open-minded and, after some discussion, understood why it was essential to have burial insurance.

So, try not to panic. Odds are your parents will appreciate that you considered their feelings on the matter.

Step #2 – Understand What You’re Looking For

Technically, this step goes hand in hand with step #1.

Understanding what you’re looking for in a burial life insurance plan is critical to sorting out the best coverage that suits your situation.

For instance, do your parents want to be buried or cremated? Understandably, this can be a difficult question to ask. But depending on the funeral arrangements they’d prefer, there can be a considerable price difference.

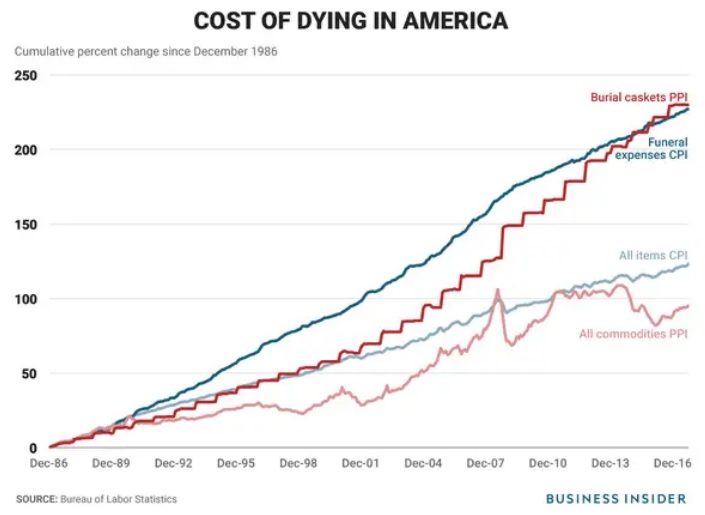

In the United States, burial and cremation costs are steadily increasing far above the average inflation rate. Take a look at the chart below.

You can easily see that funeral costs, on average, are increasing at a faster rate than the average price of everything else.

According to the National Funeral Directors Association, the average burial cost is approximately $9,135 while the average cremation cost is roughly $5,150.

Keep in mind this amount can vary across the country, depending on whether you live in a high or low cost-of-living state.

Either way, funeral costs are on the rise, so it makes sense for families to take out more coverage than they think they need.

What my Mom and I selected

When I had this conversation with my mother in 2012, we chose a $15,000 burial insurance plan, even though all she wanted was a basic cremation. We felt this amount was necessary to help cover unforeseen expenses.

Just like your parents, my mom didn’t want to burden us with any final expenses. She wanted to guarantee there was more than enough coverage available, which is exactly what I advise my clients to do.

Step #3 – Thoroughly Discuss Your Parent’s Health

When your parent applies for most types of burial insurance policies, it’s highly likely that she must answer health questions.

To be honest, as long as your parent’s health isn’t terrible, health questions can be beneficial. Assuming you can reply “NO” to everything, health questions allow you to apply for better quality coverage.

As a side note, keep in mind that there are “guaranteed acceptance, no questions asked” insurance plans. There are some limitations to these plans. But they are a great choice when there are no other options available due to health issues.

What health questions should you ask?

Here’s a list of health issues to discuss with your parents:

- Heart attacks

- Stroke

- Stents

- Bypass

- Seizures

- Aneurysms

- Pacemakers

- Congestive

- Heart failure

- Lung disease

- COPD

- Diabetes

- Kidney/liver problems

- Mental health issues

- Oxygen supplemental usage

- Cancer history

Also, make sure you ask your parent to review all of the prescriptions that they take.

Burial insurance specialists must catalog both health history and prescription usage.

I remember sitting down with my mother and asking her about her health history. My mother’s a very reserved person.

Nevertheless, she knew that answering these questions was necessary for securing a good burial insurance policy. That’s why you should strive to get your parent to do the same.

Step #4 – Choose the Right Agent: Captive or Independent?

You could go and buy a burial insurance plan directly from a company like Mutual of Omaha, AARP, or Colonial Penn.

However, we call these companies “captive agencies.”

What’s a captive agent?

Agents who are captive will only push their employer’s products regardless of what’s best for their clients.

Captive agents typically recommend what’s called term insurance (insurance that cancels after a specific date) or offer limited plans that don’t cover natural death for the first two years.

That’s why I believe you should work with an independent agent.

How independent agents work

An independent agent has access to a multitude of carriers (not just one provider!).

In other words, they have a far better chance of finding quality coverage that suits your needs.

As an independent agent myself, I aim to find the best burial insurance for my elderly parent clients – coverage that’s both competitively priced and (if possible) includes natural death from day one.

Step #5 – Choose the Right Product

There’s a variety of different insurance products available, and picking the wrong one can have devastating consequences.

Term Insurance

For instance, as we briefly mentioned above, your parent could outlive the burial insurance plan if you pick a term insurance plan.

Companies like AARP and Globe Life Insurance are known to push term insurance since it’s the main product they sell.

But if your mom or dad outlives the plan, they lose everything! No coverage. No payout.

What’s worse? Now your parents are even older with NO burial insurance coverage in place. In this situation, it becomes a lot harder to secure quality, affordable life insurance.

Whole Life Insurance

Another option you could consider is whole life insurance.

This coverage never cancels due to age or health. And in some cases, we can secure first-day full natural death coverage (if the client qualifies).

This is the crème-de-la-crème of coverage. When I got my mother a burial insurance policy, whole life insurance was the natural decision.

Knowing that your parents are covered whenever they pass away is a huge relief. Plus, you don’t have to worry about the price increasing since whole life insurance premiums never go up.

Step #6 – Exam or No Exam?

You need to decide whether or not you want your parent to take a medical exam.

Most clients we talk to do not. The exam is an exhausting process, and underwriting is extremely tough for people in their advanced years.

The good news is that if you work with us at Buy Life Insurance For Burial, we can access carriers that don’t require any examinations whatsoever!

All your parents need to do is complete an application and agree for us to check their medical records and prescription history.

The process is simple. And we usually get a result within minutes after applying!

When exams are necessary

If your parents are incredibly healthy and you’re interested in securing a substantial amount of coverage (over $50,000), an exam is most likely required.

However, in my experience, this is rarely the case. But, this is an option if it’s something you’re interested in considering.

Step #7 – Determine Payment Beneficiary

At this point, you’ve probably already figured out who’s going to handle the premium payments.

Our only recommendation is that if you decide to pay the premium, set up the payment from YOUR bank account.

You don’t want to be in a position where you have to send money to your mom or dad each month. It adds another complication to the process that, in our experience, is best avoided.

However, if your parents decide that they want to pay for the insurance plan, they can. My mother wanted to take care of the payments, so we set up the payment plan in her name.

Step #8 – Who Should the Beneficiary Be?

Make sure you discuss who should receive the money after your mom or dad passes. We recommend choosing someone who can handle organizing your parent’s funeral arrangements.

Also, make sure to add a contingent beneficiary. This is the “backup” beneficiary if the first beneficiary dies before your parent.

Step #9 – Complete the Application

This is a pretty simple step since the agent will complete it for you. However, there are multiple “sub-steps” involved.

First, we have to:

- gather your parent’s information,

- input the data into the system,

- confirm their signature, and,

- set up the payment schedule.

Clear communication and coordination between the agent, child, and parent will help speed up the process.

If the child and parent aren’t simultaneously available to complete the application, it can really slow the process down.

Step #10 – Getting a Policy

If everything has gone according to plan, you’ll receive approval of your parent’s burial insurance plan instantly or a couple of days after applying.

However, sometimes things don’t work out as planned. That’s why at Buy Life Insurance For Burial, we teach our agents to always have a backup in place.

For example, we have access to multiple carriers that can act as great backup options when your first choice doesn’t work out.

Once approved, the insurer will receive the policy in the mail. This can take several weeks. Make sure you review all the information covered in the plan once you receive a paper copy.

Lastly, it’s also a good idea to store the document in a safe place so you can refer back to it when you need to.

Get a Free Quote

I hope this guide has helped you understand the process of getting burial insurance for your parents.

If you’re looking for a free, no-obligation burial insurance quote for your mom or dad, we can help!

Our team of trusted professionals frequently help adult children secure quality, affordable burial insurance for their parents.

Call us directly right now at:

888-626-0439

We can run a quote for you in under ten minutes.

Or, to submit a quote request online, you can also click the “quote request” button at the top or side of your screen.

Thank you for reading!